- IOLTA in Louisiana – Louisiana requires attorneys to use IOLTA (Interest on Lawyers’ Trust Accounts) for holding client funds that are nominal or short-term, with interest benefiting the Louisiana Bar Foundation. Strict state bar rules mandate how these trust accounts are managed. Learn how to set up an IOLTA checking account.

- Trust Compliance Principles – No commingling of client funds with firm money, detailed recordkeeping (individual client ledgers, five-year retention), regular reconciliation (at least quarterly by rule), and proper handling of earned vs. unearned fees are all critical.

- LeanLaw for Trust Accounting – LeanLaw’s legal accounting software, integrated with QuickBooks Online, automates three-way reconciliations and provides real-time client ledger visibility, helping Louisiana firms stay compliant with bar regulations effortlessly.

What Is IOLTA and Why It Matters in Louisiana

IOLTA (Interest on Lawyers’ Trust Accounts) is a program that pools client funds held by lawyers in trust, and uses the interest to fund legal aid and justice programs. In Louisiana, IOLTA is mandatory – any lawyer or firm that holds client funds must participate. This means if you handle client money (settlements, retainers, court fees, etc.), you must have an IOLTA trust account at an approved, FDIC-insured bank. Funds that are “nominal in amount or to be held for a short period” go into the IOLTA account, and no interest from these accounts can benefit the lawyer or client – the interest is paid to the Louisiana Bar Foundation by rule.

Why does IOLTA matter? Aside from the ethical obligation, it’s also about fairness and compliance. Before IOLTA programs, lawyers would hold client funds in non-interest accounts, meaning neither client nor public benefited from the interest. With IOLTA, those pennies of interest add up to support access-to-justice in the state. For Louisiana firms, participating in IOLTA is not optional – failure to use an IOLTA for eligible funds violates Louisiana Supreme Court rules. Moreover, each state has its own IOLTA rules, so Louisiana firms must follow Louisiana’s specific requirements.

Importantly, not all client money belongs in IOLTA. If a client’s funds are substantial in amount or will be held long enough to earn net interest for the client, you should place those in a separate interest-bearing trust account for that client (with the interest going to the client) rather than in IOLTA. The Louisiana rules guide attorneys to consider factors like the amount and duration when deciding between IOLTA vs. a dedicated interest-bearing account for a client. Failing to do so could deprive the client of interest they’re entitled to.

From an accounting perspective, IOLTA and trust accounts ensure that client funds are treated properly on the books. According to generally accepted accounting principles (GAAP), client trust funds are not revenue to the firm – they are liabilities that the firm holds for the client. So, these funds must be kept separate from the firm’s operating finances. By segregating these monies in a trust account (IOLTA or otherwise), a law firm can clearly account for them as client funds held in escrow, not as the firm’s income. This protects the client’s money and also ensures the firm’s financial statements are accurate and compliant with GAAP and legal ethics rules.

Core Principles of Trust Accounting Compliance

Every Louisiana law firm handling client money must adhere to core trust accounting principles. The Louisiana State Bar and Rules of Professional Conduct lay out strict guidelines to protect clients’ funds. Here are the fundamentals:

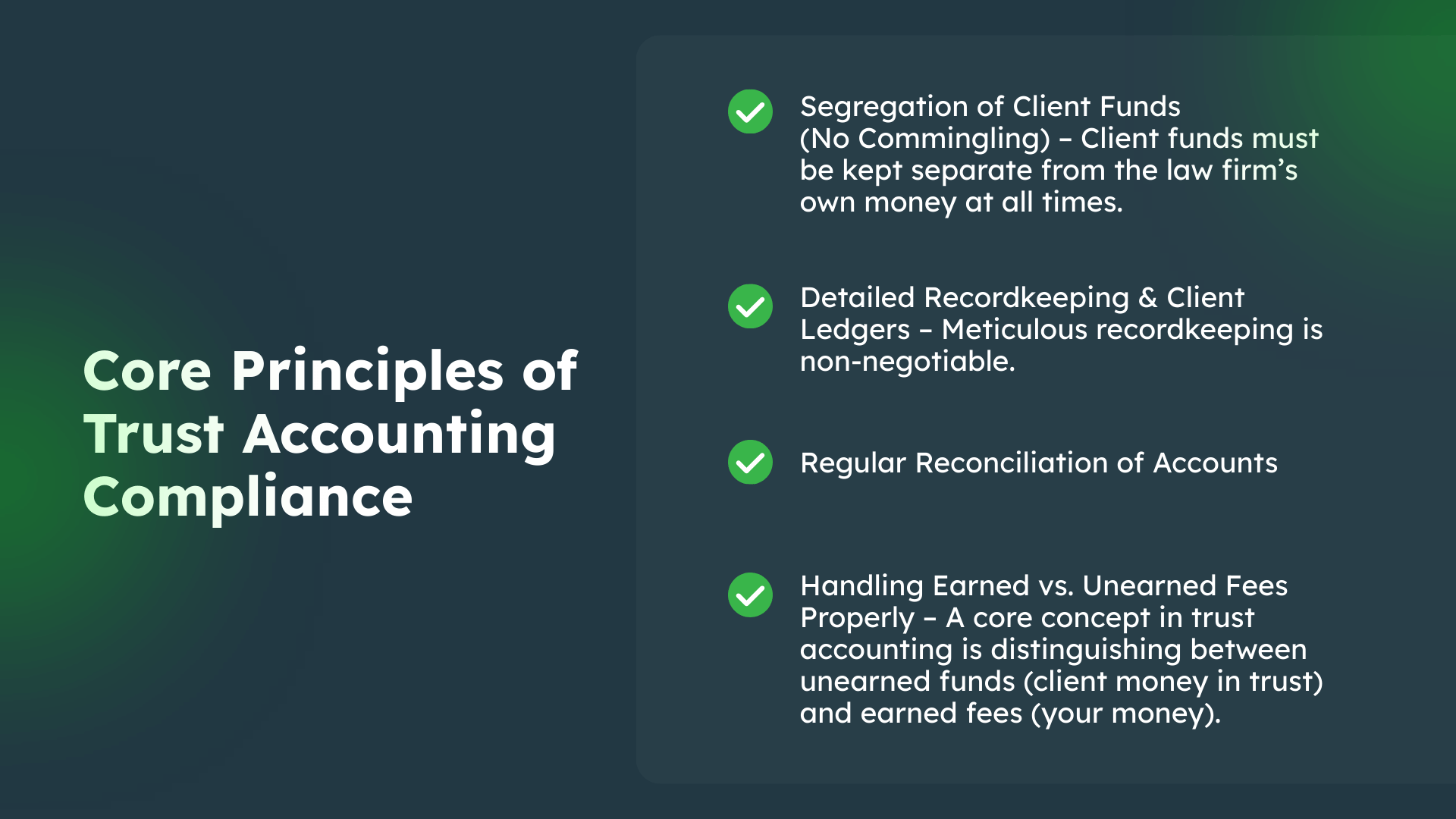

- Segregation of Client Funds (No Commingling) – Client funds must be kept separate from the law firm’s own money at all times. This means using a dedicated trust account (or accounts) for client money. You should never deposit client payments meant for future fees or costs into your operating account – if the fee isn’t earned yet, it belongs in trust. Commingling – mixing client funds with firm funds – is one of the gravest violations in trust accounting. Louisiana considers commingling a serious disciplinary offense, as it blurs the line between client property and your own. The only exception is that lawyers may keep a nominal amount of firm money in the trust account solely to cover bank service charges (e.g. to avoid monthly fees). Anything beyond that is not allowed. By keeping each client’s funds segregated in the trust account, you uphold your fiduciary duty and avoid even the appearance of using client money for personal or firm expenses.

- Detailed Recordkeeping & Client Ledgers – Meticulous recordkeeping is non-negotiable. You must maintain a complete ledger for each client whose funds you hold, showing every deposit, withdrawal, and remaining balance for that client. Whenever money goes in or out of the trust account, record the date, amount, client matter, and purpose. Good practice is to immediately update the client’s ledger and keep a corresponding master ledger for the whole account. Louisiana rules mandate that lawyers preserve complete records of trust account funds for at least five years after the representation ends. These records include bank statements, cancelled checks, deposit slips, wire confirmations, client instructions, invoices, and settlement statements – essentially anything related to trust transactions. In the event of an audit or client inquiry, you should be able to produce a clear paper trail for every penny. Transparency is key: you must be able to render a full accounting to the client (or third-party, like a lienholder) upon request. Maintaining organized records not only keeps you compliant but also builds client trust, since clients know you can account for their money at all times.

- Regular Reconciliation of Accounts – Reconciliation is the process that ensures your trust account records match the actual bank balance and that each client’s ledger is accurate. Louisiana explicitly requires trust account reconciliation at least quarterly by rule, and best practice is to reconcile monthly. A typical reconciliation means: at the end of the month, compare the trust account bank statement with your internal ledger balances, and also ensure that the total of all individual client ledger balances equals the overall account balance. This three-way check (bank balance = total of client ledgers = balance per your accounting books) is the gold standard of trust accounting. Regular reconciliation will catch errors or oversights early – for example, if you recorded a transaction incorrectly or a bank fee was taken. Louisiana’s malpractice insurer notes that reconciling client trust accounts diligently (at least each quarter, if not monthly) is critical to minimize the risk of an overdraft and to spot any discrepancies. In fact, under Louisiana Supreme Court Rule 19, banks must notify the Office of Disciplinary Counsel (ODC) of any trust account overdraft. If your trust account is even one dollar short of what it should hold for clients, it signals a serious problem (potentially conversion of funds). By reconciling frequently, you ensure that client funds are always intact and correct any mistake before it becomes a compliance breach. Always document your reconciliations (keep reports), and if you find and fix an error, keep notes – this shows good faith efforts at compliance.

- Handling Earned vs. Unearned Fees Properly – A core concept in trust accounting is distinguishing between unearned funds (client money in trust) and earned fees (your money). Louisiana ethics rules (Rule 1.5(f)) and generally accepted accounting principles both say that money you receive before it’s earned must stay in the trust account until you earn it. For example, if a client gives you a $5,000 advance for hourly work, that entire amount is unearned initially and goes into trust. As you perform the work and bill the client, you can then pay yourself the earned portion from the trust account (typically by transferring that amount to your operating account) only when it’s earned and with proper documentation (like an invoice or billing statement to the client). Unearned funds are client property – using them prematurely is effectively borrowing the client’s money. On the flip side, once you have earned fees and billed the client for them, you should promptly remove that money from the trust account (after notifying the client via an invoice) and move it to your firm’s operating account. Failing to withdraw earned fees on a timely basis can lead to unintentional commingling – because those earned funds (now your money) would be sitting mixed in the trust alongside other clients’ funds. The Louisiana State Bar’s guidance even suggests a best practice: don’t pay yourself until after the client’s share and any third-party payments are disbursed, but then do pay yourself promptly. In summary, treat the trust account as sacred: it holds client money only (unearned fees, advances, settlement portions for client/third parties), and the firm’s earnings should only touch the trust account when moving out the earned amount, not as a holding account. Always provide the client with clarity – typically via an invoice or settlement statement – showing how much was earned and is being transferred out of trust. This keeps you aligned with both ethical rules and sound accounting (revenue recognition) practices.

By mastering these core principles – segregation, recordkeeping, reconciliation, and proper handling of unearned vs. earned funds – Louisiana firms can maintain ironclad trust compliance. These aren’t just bureaucratic rules; they are protections for your clients and for your firm. Mishandling client funds can lead to client loss, malpractice claims, or worse, disciplinary action and damage to your reputation. On the other hand, a clean trust account instills confidence and lets you focus on practicing law, not worrying about an audit.

How LeanLaw Simplifies Trust Accounting Compliance (for Louisiana Firms)

Managing trust accounting manually – with spreadsheets, paper ledgers, and manual bank reconciliations – can be tedious and error-prone. This is where legal-specific accounting software like LeanLaw comes in. LeanLaw is designed to take the headache out of trust accounting and ensure compliance with both general accounting standards and Louisiana’s state bar rules. Here’s how LeanLaw’s trust accounting features help Louisiana firms stay on top of their IOLTA and trust obligations:

- Streamlined Trust Transactions (Earned Fee Transfers and Payments): LeanLaw simplifies the process of moving funds in and out of the trust account in a compliant way. For example, when you complete work and want to pay an invoice using the client’s trust funds, LeanLaw’s integrated invoicing workflow makes it easy. You can apply the trust funds to the invoice with a few clicks, and LeanLaw will automatically deduct the amount from the client’s trust balance and record the transfer to your operating account in QuickBooks. This ensures you only withdraw what has been billed (i.e. earned) – which helps enforce the rule that unearned money stays in trust until earned. It effectively builds the “earned vs. unearned” safeguard into your billing process. What might be a multi-step, error-prone process to do manually in QuickBooks (creating journal entries or cutting checks from trust for each invoice) becomes nearly foolproof with LeanLaw. The same goes for making trust deposits – LeanLaw guides you to record them properly to a client’s ledger, so you don’t accidentally code a retainer deposit as income. With LeanLaw, all trust receipts and disbursements are handled in a way that keeps the accounting clean: trust receipts increase the client’s liability balance, trust payments reduce it and correspondingly move funds to income or to a payee as appropriate. This level of automation and control means less chance of human error that could violate trust accounting rules.

- Integration with QuickBooks Online (No Double-Entry): Because LeanLaw is deeply integrated with QuickBooks Online, it acts as a legal-specific layer on top of robust general accounting software. All your trust account transactions entered in LeanLaw sync to QuickBooks in real time, updating your financial statements and bank registers. Likewise, any activity in the bank (like interest credits or bank fees) can be synced back. This eliminates the need to enter data twice or manage complex spreadsheets to mirror your trust accounting. By using LeanLaw with QuickBooks, Louisiana firms get the best of both worlds: legal ethics compliance (through LeanLaw’s safeguards and legal-specific workflows) and GAAP-compliant bookkeeping (through QuickBooks’ general ledger and reporting). The integration ensures that your trust account in QuickBooks is always accurate and matches what LeanLaw shows, which in turn should match the bank – thereby naturally producing the required three-way reconciliation with minimal effort. In short, LeanLaw automates the heavy lifting of trust accounting so that your firm can focus on clients, not balancing checkbooks. As LeanLaw’s own materials put it, “trust accounting is effortless and error-free” with an automated system ensuring you adhere to state bar standards. This level of reliability is especially valuable in Louisiana, where any mistake in handling client funds can trigger regulatory scrutiny.

By leveraging technology like LeanLaw, even a small firm with limited administrative staff can maintain big-firm-quality accounting controls. For Louisiana attorneys, this means peace of mind: your IOLTA and trust accounts stay compliant with Louisiana State Bar rules and generally accepted accounting principles, virtually on autopilot. LeanLaw essentially serves as a built-in safety net, preventing common trust accounting mistakes (overdrafts, commingling, math errors) before they happen and providing a clear audit trail of every client dollar. Given that commingling and misappropriation of client funds are leading causes of attorney discipline in Louisiana, using these tools can be a game-changer. It’s not just about avoiding discipline either – it’s about running a more efficient practice. When your trust accounting is clean and automated, you build a reputation for integrity and you free up time that can be spent serving clients rather than wrestling with bank statements.

(Internal Link: For a deeper dive into how LeanLaw and QuickBooks work together for trust accounting, see LeanLaw’s guide on legal trust accounting in QuickBooks Online which compares the “hard way” vs. “easy way” of managing trust funds.)

Common Pitfalls in Managing Trust Accounts (and How to Avoid Them)

Even with rules and tools in place, law firms can fall into some common trust accounting traps. Here are some frequent pitfalls Louisiana small and mid-sized firms face in managing IOLTA and trust accounts – along with tips to avoid them:

- Commingling Firm and Client Funds: One of the most dangerous missteps is commingling, which happens when firm money and client money mix in the same account. This might occur if an attorney deposits a client’s retainer directly into the firm’s operating account (treating it as immediate income), or leaves earned fees sitting in the trust account alongside client funds. In Louisiana, commingling is strictly prohibited and viewed as a serious ethics violation. Avoid it by always using a proper trust account for client funds. Educate your staff that client money never goes in operating accounts, and firm money (except a small amount for bank fees) never stays in trust accounts. If you accidentally receive a trust check made out to the firm, don’t just deposit it in the general account – route it into trust until it’s earned. Using software like LeanLaw can help by segregating funds on the ledger and flagging you if you attempt to record something improperly. The mantra is: “If it’s not earned, it’s not yours yet.” Keep those dollars in trust.

- “Borrowing” from the Trust Account (Conversion): A step beyond commingling is conversion, which is using client funds for something other than that client’s matter – even temporarily. Some lawyers under financial pressure have rationalized using one client’s money to pay another expense, intending to “pay it back later.” This is highly dangerous. Louisiana ODC and courts treat misappropriation of client funds as one of the most serious forms of misconduct, often warranting disbarment. Even if the misuse is short-term or due to negligence (e.g., you forgot a check had cleared and accidentally overdrew the trust), it’s still conversion. Never treat the trust account like a cushion for cash flow problems. As the CNA risk bulletin warns, conversion can occur “even if the lawyer had no dishonest motive” – for example, a math mistake or a bounced deposit can technically convert other clients’ funds. The best prevention is to treat the trust account as sacrosanct. Don’t tap it for any reason other than proper disbursements. Monitor balances closely so you don’t accidentally dip below what you should be holding. If you find yourself even thinking about “borrowing” from client funds, stop and seek another solution (like a bank line of credit) – the risk to your license is simply not worth it. Remember, issuance of an NSF (bounced) check on a trust account automatically signals possible conversion of funds and will trigger an inquiry. Keep an adequate cushion of your own money in operating accounts so you’re never tempted to reach for client funds.

- Inadequate or Irregular Reconciliation: Another pitfall is failing to reconcile the trust account regularly, which can let small errors snowball into big problems. If you’re not reconciling, you might not notice that you recorded a $1,000 deposit for John Doe when it was actually for Jane Doe, or that a bank fee pushed one client’s sub-balance negative. Neglecting reconciliation is risky enough that Louisiana requires at least quarterly reconciliations by rule. But waiting three months is not ideal – by then a mistake could have compounded. Avoid this pitfall by reconciling the trust account every month. Many firms even reconcile weekly, especially when volume is high. Set a calendar reminder or use an accounting tool that essentially reconciles in real-time (LeanLaw, for example, keeps running balance checks). When reconciling, don’t just compare the bank statement to the overall balance – also ensure each client’s ledger balance is correct. This “triple reconciliation” confirms no client’s funds are inadvertently in the red. If you discover any discrepancy, investigate immediately. Common issues include bank errors, a transaction recorded to the wrong client, or timing differences with deposits. By reconciling frequently, you catch these before they become compliance violations. Moreover, demonstrating a regular reconciliation process is a strong defense in case the Bar ever questions your practices – it shows you are being a careful steward of client money.

- Disbursing Funds Too Early (Floating Funds): Timing is critical in trust accounting. A frequent error is disbursing funds from trust before a corresponding deposit has fully cleared the bank. For instance, you receive a settlement check and deposit it today, then immediately cut checks to the client and lienholders tomorrow. If that settlement check bounces or is delayed, you’ve now paid out money that wasn’t actually there – effectively using other clients’ funds to cover the shortfall. Louisiana bar guidance explicitly warns: “A check deposited into trust should clear prior to any disbursement of those funds. The risk that a draft may not clear should not be borne by other clients.” Using the “float” (paying out in anticipation of a deposit clearing) is treated as conversion of the other clients’ funds. To avoid this, always wait for confirmation that funds have cleared before disbursing. For paper checks, that may mean 3-5 business days – your bank can confirm clearance. With wire transfers or certified funds, clearance is usually same-day, but verify if unsure. Communicate to clients that there is a short holding period for any check deposit to clear (the LSBA suggests telling clients about the 3-5 day clearing window). This sets proper expectations and protects you. Also, never write trust checks against uncollected funds. If timing is an issue (e.g., a client needs their money ASAP), consider options like asking the paying party to wire the funds or using a service that can instantly verify the availability of funds. But under no circumstances should you spend money that isn’t securely in the trust account.

- Mishandling Advance Fees and Retainers: Many Louisiana lawyers receive advance fee retainers or flat fees. A pitfall is treating these advances improperly – either leaving them in operating (as if immediately earned) or, conversely, not withdrawing them from trust once earned (which results in commingling). Louisiana’s rules (and Rule 1.5(f)) are clear that advance fees belong in trust until earned. So the moment you receive a retainer, record it in the trust account under that client’s ledger. As you perform work, invoice the client. Then you can pay the invoice from the trust funds. Failing to invoice regularly can lead to a situation where you’ve done the work but still have large sums in trust that are technically yours – which you shouldn’t leave co-mingled with client funds. The flip side is even worse: using advance fee money before you’ve earned it (without client permission) is basically borrowing the client’s money. The avoidance strategy here is to diligently track work in progress and bill on a regular schedule (e.g., monthly). Each time you bill, use that as a trigger to move the earned amount from trust to operating (and inform the client). Modern legal billing software can help automate this by linking time entries to trust withdrawals. Also, make sure any engagement letter aligns with Louisiana’s rules – if you charge a flat fee and intend it to be earned on receipt or at specific milestones, the agreement must comply with Rule 1.5(f) requirements (for example, flat fees can sometimes be treated as earned upon receipt only if certain disclosures are made, etc., but that’s beyond our scope here). The safe approach: when in doubt, put it in trust and only take it out as you earn it. If a client ends the representation early, promptly refund any remaining unearned amount from the trust.

- Lack of Internal Controls and Oversight: Small firms sometimes operate on trust – literally and figuratively – by having one person (perhaps a paralegal or the office manager) handle all trust accounting with little oversight. This can lead to innocent mistakes going unchecked or, in worst cases, intentional misappropriation (embezzlement) by an unscrupulous employee. Common pitfalls include allowing non-lawyers too much unsupervised access to trust funds or using convenience methods that bypass controls (like debit cards). In Louisiana, all trust checks must be signed by a lawyer – you should not pre-sign trust checks or hand out a signature stamp. Likewise, debit card withdrawals or ATM access to trust accounts are forbidden, because they make it too easy to withdraw cash without proper records. To avoid internal control issues, implement a few best practices: require dual signatures for large trust disbursements, review trust accounting reports monthly (even if you don’t do the daily bookkeeping, the responsible attorney should review what the bookkeeper has done), and segregate duties if possible (the person reconciling shouldn’t be the same person who cuts all the checks). The CNA risk management advice for lawyers suggests steps like prohibiting checks to cash, prohibiting “cash back” on deposits, not allowing any ATM withdrawals, and changing online banking passwords when staff with knowledge leave. These may seem like minor administrative details, but they go a long way. Supervise your staff – a non-lawyer can help with bookkeeping, but the attorney is ultimately responsible to ensure compliance. Regularly check the work. Many firms have a rule that any trust transfer to the operating account must be approved by a partner – which is a good check and balance. With LeanLaw or similar software, you can also easily audit who entered transactions and require approvals for certain actions. In short, maintain a healthy dose of oversight on all trust accounting activities. It’s easier to spend a few minutes reviewing a report than to deal with a disciplinary investigation later because an issue went unnoticed.

- Not Knowing Louisiana’s Specific Rules: Some pitfalls arise simply from being unaware of the quirks of Louisiana’s trust accounting rules. While most are common sense, a few Louisiana-specific requirements deserve attention. For example, attorneys must ensure their trust account is in a bank that agrees to report overdrafts to the ODC – this is typically handled by using approved “eligible financial institutions” for IOLTA, and by filing the Trust Account Disclosure and Overdraft Notification form with the Louisiana Supreme Court when you open the account. If you move your trust account to a new bank, you need to update this form. Another Louisiana requirement: if you close a trust account or open a new one, report that as well (the annual registration process will usually prompt updates). Also, Louisiana’s Rules (and LSBA guidance) explicitly forbid certain transactions (like those debit card/cash withdrawals mentioned) that might be allowed in other states – so a lawyer relocating from elsewhere must adapt to Louisiana’s stricter stance on those conveniences. Avoiding this pitfall is straightforward: familiarize yourself with Rule 1.15 of the Louisiana Rules of Professional Conduct and the LSBA’s Trust Accounting Guide. Keep a checklist of Do’s and Don’ts handy (for instance: Do reconcile quarterly; Don’t sign blank trust checks; Do keep records 5+ years; Don’t pay personal expenses from trust; etc.). The Louisiana State Bar Association provides ethics counsel who can answer questions if you’re unsure about a trust account scenario – taking advantage of that resource can prevent a misstep. Additionally, consider continuing legal education (CLE) specifically on trust accounting – these often cover Louisiana-specific traps. In sum, staying educated is key: the rules can change (for example, the requirement for quarterly reconciliations was a later addition to Rule 1.15), so keep an ear out for any updates from the Bar.

By being aware of these pitfalls and implementing safeguards to avoid them, Louisiana law firms can protect themselves and their clients. Many of the precautions boil down to diligence and documentation: pay attention to your trust account, don’t cut corners, and when in doubt, err on the side of caution with client funds. If a mistake does happen, address it immediately – for example, if you realize you’ve overdrafted the trust account or mis-deposited a check, notify the ODC proactively and correct it. It’s far better that they hear it from you first with an explanation and fix, than from the bank with no context. Ultimately, a well-managed trust account is a hallmark of a professional, responsible law practice. It not only keeps you out of ethical trouble but also gives clients peace of mind that their money is safe with your firm.

(Real World Example: In one Louisiana disciplinary case, a solo attorney’s trust account was inadvertently overdrawn, triggering an audit by the ODC. The audit uncovered sloppy accounting: the lawyer had disbursed funds to himself and others without accounting for all outstanding client liabilities, leaving the trust account balance insufficient to cover what was owed to clients and third parties. The lawyer hadn’t intended to misappropriate funds, but his poor recordkeeping led to a violation of Rule 1.15 for failing to safeguard client property. This illustrates how even unintentional mistakes – not reconciling, not tracking each obligation – can put a lawyer at risk. The takeaway: rigorous accounting and compliance checks could have prevented this nightmare.)

Frequently Asked Questions (FAQ) – Louisiana IOLTA & Trust Accounts

Q: Which attorneys are required to have an IOLTA trust account in Louisiana?

A: Virtually all Louisiana attorneys who handle client or third-party funds must maintain a trust account, and if the funds are nominal or short-term, it must be an IOLTA. The IOLTA program is mandatory for lawyers in private practice. Only those who never deal with client money (like some government or in-house lawyers) are exempt from needing a trust account. If you ever receive client funds (even a $100 filing fee advance), you need to deposit them in a trust account. Louisiana also requires you to disclose your trust account to the Supreme Court’s disciplinary authority and have your bank agree to overdraft reporting.

Q: What steps are involved in properly handling a client retainer or advance fee in Louisiana?

A: When you receive an advance fee or retainer, deposit it into your trust (IOLTA) account – not your operating account – and record it under the client’s ledger. The funds should stay in trust until you earn them by doing the work. As you bill hours or complete tasks, invoice the client. With the client’s approval (usually via the engagement agreement and the invoice), transfer the earned amount from trust to your operating account to pay your fee. Always leave any unearned portion in trust. Once the matter is concluded, promptly refund any remaining balance to the client. Essentially, treat the trust account as the holding place for the client’s money and only move it to your firm’s money once it’s actually earned (or once expenses are incurred). This practice is required by Louisiana Rules (see Rule 1.5(f) and Rule 1.15) and keeps you compliant on handling of unearned fees.

Q: How often should we reconcile our trust account, and what does a reconciliation involve?

A: Louisiana requires at least a quarterly reconciliation of your trust account, but best practice is to reconcile it monthly. A reconciliation means you verify that the bank’s record of your trust account balance matches your internal records. To do this, you’ll compare the bank statement balance to the balance per your checkbook or software ledger, and also to the total of all individual client ledger balances. All three should equal. If, for example, the bank statement shows $50,000, your QuickBooks trust account shows $50,000, and your sum of client subaccounts is $50,000, you’re reconciled. If not, you’ll need to identify the difference (maybe a check hasn’t cleared yet, or you recorded something twice by accident). Louisiana’s rule (Rule 1.15) was amended to make regular reconciliation mandatory because it’s so important for catching issues. So don’t view it as a mere suggestion – set a routine each month or quarter to do this. Using tools like LeanLaw with QuickBooks can make reconciliations easier by syncing data, but you (or your bookkeeper) should still review the reports to ensure everything lines up.

Q: Can I pay firm expenses or disbursements directly from the trust account?

A: Generally, no – you should not pay general firm expenses out of a trust account, and you should only disburse funds from trust that are for that client’s matter. For example, you wouldn’t pay your office rent or a lawyer’s salary from the trust account (that would be using client funds for firm expenses – a big no-no). You also shouldn’t pay a client’s costs from trust unless those funds are indeed being held for that purpose. What you can pay from a client trust account are things like: the client’s settlement proceeds to them, amounts to third parties that belong to the client (e.g. medical lienholders, court fees – if the money for those was in trust), or transfer of earned fees to your operating account once you’ve billed the client. The trust account is not a petty cash box or a slush fund – it’s earmarked client money. So, for instance, to pay a filing fee for a client, you would first get the money from the client (or use their retainer in trust) and then cut a check from trust to the Clerk of Court for that client’s fee. But you wouldn’t pay a fee for Client A out of Client B’s funds. Each disbursement must be clearly linked to the client whose money is being held. As a rule, never withdraw more for a client than that client has in their trust balance – doing so means you’ve used other clients’ money (even if by accident). Modern practice management software can prevent that by warning of low balances. Also, remember in Louisiana you cannot withdraw cash from a trust account or use a debit card. All payments should be made by check or electronic transfer that can be documented, and checks should be payable to specific payees (never to “Cash”).

Q: What happens to the interest on an IOLTA account?

A: In an IOLTA, the interest does not go to you or your clients. By design, the interest earned on a Louisiana IOLTA trust account is remitted to the Louisiana Bar Foundation (LBF) to fund civil legal aid programs. The bank usually handles this automatically: they calculate the interest on the account (after allowable bank fees) and send it to the Bar Foundation, typically on a quarterly basis. You as the attorney don’t have to do anything to transfer the interest – except ensure your account is set up correctly as an IOLTA. Note that because of this, the interest is not taxable to you or the clients. It’s also why only nominal or short-term funds go into IOLTA – the client isn’t losing any meaningful interest because if the funds could earn net interest, you’d put them in a separate account for the client. If you ever mistakenly accrue interest to the trust account (say the bank didn’t code it as IOLTA and you get a small interest deposit), that interest is client property or must be paid to the Bar Foundation – you should correct the account setup. In summary: with IOLTA, interest is for the public good, not for the lawyer or client. This is mandated by the Louisiana Supreme Court’s rules governing IOLTA.

Q: How can small firms ensure trust compliance without a full-time accountant on staff?

A: Small and mid-sized firms in Louisiana can absolutely manage trust accounts effectively by combining clear procedures with the right software tools. First, make sure you and your team know the Louisiana rules and have a basic procedure manual (even a checklist) for trust transactions. Then, leverage technology: accounting software (like QuickBooks Online) coupled with legal-specific software (like LeanLaw or similar) can automate many aspects of trust accounting. These tools will create the necessary separate ledgers, perform calculations, and even do part of the reconciliation work for you. For example, LeanLaw will continuously sync your trust account activity and flag issues, essentially acting as a built-in accountant watching the trust. Even without specialized software, a small firm should at minimum use QuickBooks or another ledger to track trust funds (trying to do it purely by hand is inviting errors). Schedule a dedicated time each month to review the trust account – it could be just an hour of going through a reconciliation report and scanning the client balances for anything unusual. Many banks in Louisiana offer IOLTA account analysis statements that detail all transactions and interest, which you can cross-check against your records. If you don’t have an internal accountant, consider hiring a part-time bookkeeper or utilizing an accounting service familiar with law firm trust accounting. Outsourcing the monthly reconciliation to a CPA or bookkeeping service can be cost-effective and adds a layer of assurance. Finally, avail yourself of bar resources: the LSBA’s Practice Aid Guide on trust accounting (Section 3 on their website) is a great reference, and LSBA’s ethics counsel can answer questions. In short, even without full-time staff, small firms can stay compliant by using software to automate tasks and committing to regular oversight. It’s all about establishing a routine – once that’s in place, trust accounting will feel much less daunting.