- Utah’s IOLTA rules require law firms to hold client funds in special trust accounts: All Utah attorneys who handle client funds must use an Interest on Lawyers’ Trust Account (IOLTA) at an approved bank. These interest-bearing trust accounts pool client money, with interest automatically sent to the Utah Bar Foundation to fund legal aid. Strict state bar rules mandate segregation of client funds, detailed recordkeeping, and regular reconciliations to ensure compliance.

- Mismanaging trust accounts is a leading cause of discipline in Utah: Trust accounting violations – like commingling client money with firm funds or failing to account for client fees – frequently result in ethics complaints. Nearly 10% of lawyers nationally have faced disciplinary action over trust fund mishandling. Utah’s Office of Professional Conduct (OPC) actively monitors trust accounts (banks must report any bounced trust checks), and penalties for violations range from reprimands to suspension or disbarment.

- Legal billing software can simplify IOLTA compliance: Modern tools like LeanLaw automate trust accounting tasks so small firms can meet Utah’s requirements with ease. LeanLaw’s cloud-based system provides three-way reconciliation of bank, trust ledger, and client ledgers in real time, one-click trust disbursements when invoicing, and robust client ledger reporting – all aligned with Utah’s bar standards. By using dedicated legal billing software, Utah firms can avoid common mistakes, stay audit-ready, and focus on clients instead of chasing spreadsheets.

Understanding Utah’s IOLTA Program and Trust Accounting Rules

What is IOLTA? IOLTA stands for Interest on Lawyers’ Trust Accounts. It’s a program established by the Utah Supreme Court in 1983 that requires attorneys to deposit qualifying client funds into a pooled, interest-bearing trust account. Qualifying funds usually mean client money that is small in amount or held for a short time – funds that couldn’t earn interest for the client net of bank fees. Rather than sitting idle, the interest from these pooled accounts is remitted to the Utah Bar Foundation to support civil legal aid programs. In this way, Utah lawyers collectively help fund access-to-justice initiatives every time they hold client money in trust.

Mandatory participation and approved institutions: Utah’s IOLTA compliance is not optional. If you’re a Utah attorney handling client money – whether advance fee retainers, settlement funds, or court fees – you must use an IOLTA trust account. The account must be opened at a financial institution approved by the Utah State Bar (institutions that meet requirements and agree to remit interest to the Bar Foundation). Utah-approved IOLTA banks typically offer familiar banking services but with special reporting to ensure interest payments and overdrafts are handled properly. Tip: When opening the account, use the proper account naming conventions (e.g. “Trust Account – [Attorney/Law Firm Name] IOLTA”) so it’s clearly identified as a client trust account.

Utah’s safekeeping rules (RPC 1.15): Beyond establishing an IOLTA, Utah attorneys must follow strict Rules of Professional Conduct for safeguarding client property (Utah RPC 1.15, modeled on the ABA Model Rule 1.15). In practice, these rules mean:

- No commingling of funds: Client money cannot be mixed with the law firm’s own funds. It must stay in the trust account until earned or disbursed for the client’s matter. The only exception is a minimal amount of firm funds that may be allowed to cover bank fees, per state bar guidelines. The OPC notes that Rule 1.15 violations often arise from lawyers failing to keep their own earned fees separate from clients’ money. In short, don’t borrow or “advance” yourself money from the trust – even temporarily. Every dollar in the trust account should belong to a client until you’ve earned it and properly documented a withdrawal.

- Detailed recordkeeping and accounting: Utah lawyers must maintain complete records of all trust account transactions. Each deposit or withdrawal should be documented with the date, amount, source or payee, client matter, and purpose. You should maintain a client ledger for each client showing all funds held on their behalf, as well as an overall trust ledger for the account. Utah’s rules (again echoing ABA standards) require that you be able to account for every penny in the trust account at any given time. Good practice is to provide clients with receipts or ledger statements when you receive funds and when you make payments out of trust on their behalf. Also, under Utah’s rules, trust account records should generally be retained for a number of years after the representation (five years is a common standard) in case of audits or questions down the line.

- Proper use of funds & prompt distribution: Funds in a trust account can only be used for their intended client-specific purpose – nothing else. For example, if the money is a retainer for fees, you may transfer those funds to your operating account only after you have earned them (typically by invoicing the client for work performed). If the funds are for a real estate closing or settlement, they should be disbursed to the proper payees (client, lienholders, etc.) according to the settlement terms. Don’t delay disbursing funds longer than necessary – Utah expects prompt notification and delivery of funds to clients when due. Likewise, if a client requests a refund of an unused retainer, you must promptly return it from the trust account. Failing to promptly account for and deliver client funds is another common pitfall that can lead to ethics complaints.

- Regular reconciliation: A critical compliance step is reconciling the trust account regularly (ideally monthly). Reconciliation means comparing three key records: (1) the bank statement balance (adjusted for any outstanding checks or deposits), (2) the total of all clients’ trust ledger balances added up, and (3) the balance per your own trust ledger. A proper three-way reconciliation ensures all three figures are identical. If they aren’t, you must find and correct the discrepancy. Utah regulators expect attorneys to perform such reconciliations on a schedule (monthly is best practice) and to keep documentation. Regular reconciliations help catch errors like bank fees being charged, a deposit recorded to the wrong client ledger, or a check that hasn’t cleared. By catching and correcting issues early, you prevent minor mistakes from snowballing into serious violations.

Utah’s Office of Professional Conduct (OPC) oversight: The OPC is the disciplinary arm that enforces these rules. Utah has a particularly vigilant system: banks must notify the OPC whenever a trust account check is presented against insufficient funds (NSF) – even if the bank honors the check. In 2023 alone, Utah’s OPC opened 31 new investigations due to trust account NSF notices. The vast majority of these incidents turned out to be bookkeeping errors or timing issues (e.g. a deposit that hadn’t cleared yet). However, each notice triggers an inquiry, and patterns of problems will draw closer scrutiny. The OPC has also identified trust account mismanagement as a recurring issue in disciplinary cases. According to the OPC’s annual report, Rule 1.15 violations often stem from lawyers not segregating client funds or failing to account for how client money was spent. In ethics hearings, trust accounting problems show up frequently alongside issues like communication and fee disputes.

The consequences for breaching Utah’s trust accounting rules can be severe. Depending on the misconduct, sanctions can include mandatory ethics training (trust accounting school), admonishments or reprimands (public or private), probation with audits, suspension from practice, or even delicensure (permanent disbarment) for egregious misuse of client funds. In other words, mishandling client trust money is one of the fastest ways to lose your law license. The Utah Supreme Court and Bar take these obligations extremely seriously – as do clients, who are entrusting you with their money. Fortunately, by adhering to the rules and best practices discussed here, you can avoid these risks and confidently manage your trust account.

Best Practices for Utah IOLTA Compliance and Avoiding Violations

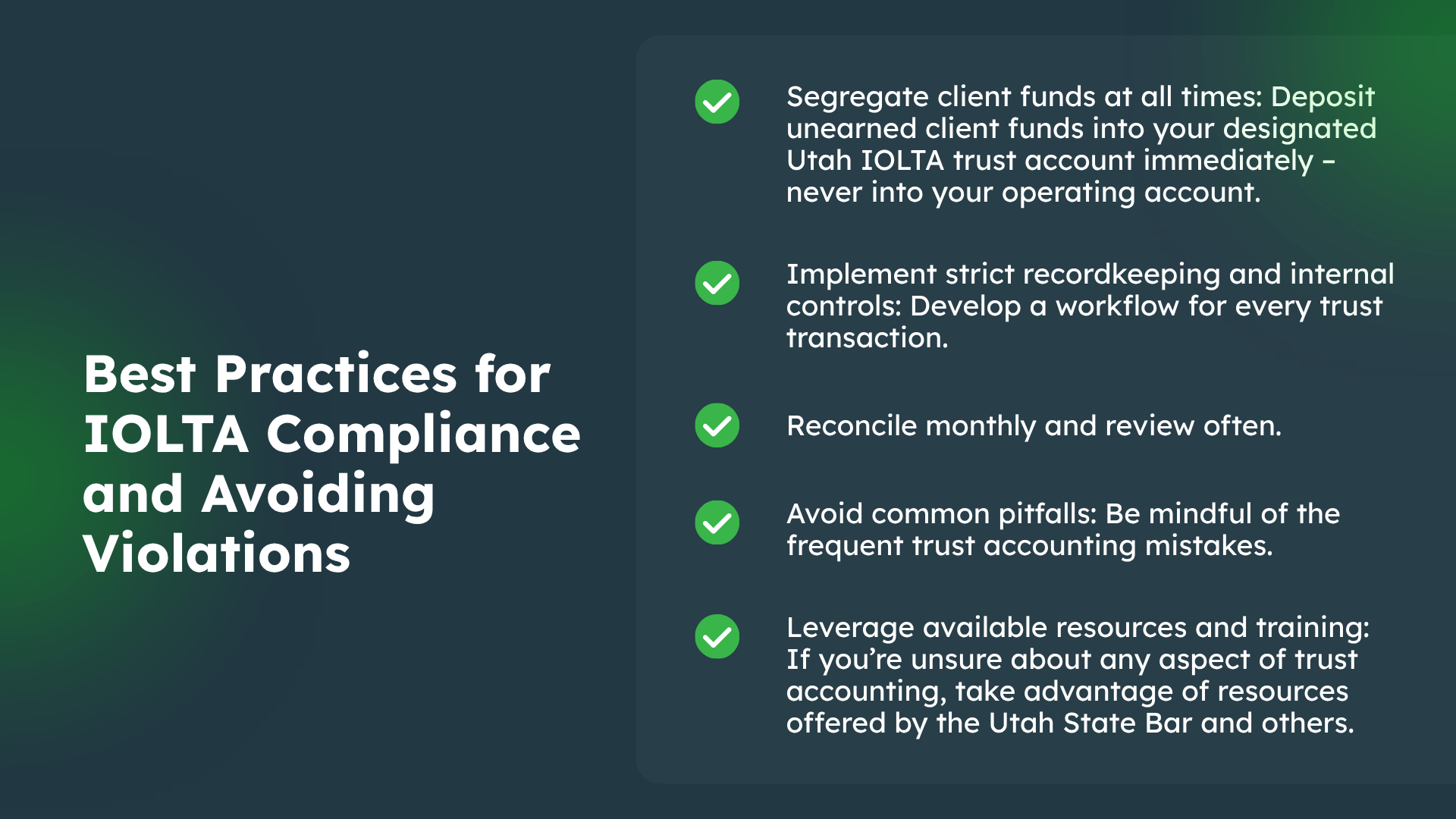

Staying compliant with IOLTA and trust accounting in Utah ultimately comes down to implementing strong business practices. Here are key best practices for small and mid-sized firms to maintain trust account compliance and avoid the common pitfalls:

- Segregate client funds at all times: Deposit unearned client funds into your designated Utah IOLTA trust account immediately – never into your operating account. Keep each client’s balance separate in your records. If you receive a check that includes both earned fees and a new advance for costs, split it between your operating and trust accounts appropriately. Never use one client’s money to cover another client’s obligations. Even if you’re a solo with one trust account, mentally treat it as multiple sub-accounts – one for each client. Modern legal accounting software (or a good spreadsheet) will let you track individual client ledgers under the one bank account. This segregation is not only required by rule, but it also protects you: you’ll always know exactly how much of the money in the account belongs to which client.

- Implement strict recordkeeping and internal controls: Develop a workflow for every trust transaction. For example, when a retainer check comes in: log it on that client’s ledger with the date, amount, and purpose (“Advance fee deposit for Case X”), give the client a receipt or invoice credit, and deposit it to the IOLTA bank account the same day. When you pay an expense or withdraw earned fees: issue a check or electronic transfer from the trust account, record it on the client ledger (with a reference to the invoice or expense), and keep a copy of the supporting document (invoice, court order, etc.). Maintain a master list or trust ledger showing the running total of funds in the trust account and update it with every transaction. Many firms designate one responsible person (e.g. the office manager or firm accountant) to oversee trust bookkeeping, and ideally require two signatures for any trust check above a certain amount as a safeguard. The goal is to create a “paper trail” such that at any moment, you can demonstrate exactly whose funds are in the trust account and why. These records will be your best defense if the OPC ever comes knocking with questions.

- Reconcile monthly and review often: As noted, performing a monthly three-way reconciliation is considered a gold standard practice. Don’t treat reconciliation as a perfunctory chore – use it as an opportunity to review your trust accounting for errors or red flags. Compare the list of client balances to the adjusted bank statement carefully. If something doesn’t match, investigate immediately (it could be a bank error, a data entry mistake, or something more serious). Regular reconciliation also helps you catch negative balances in any client’s ledger (which should never happen – a negative balance means you over-drew that client’s funds, effectively using other clients’ money). By catching that in a reconciliation, you can correct course before it triggers an NSF notice or client complaint. It’s wise for firm leadership to review the trust bank statements and reconciliation reports, even if a staff bookkeeper performs them, to add an extra layer of oversight.

- Avoid common pitfalls: Be mindful of the frequent trust accounting mistakes. One is waiting too long to move earned fees out of trust – for example, doing legal work but not billing promptly, resulting in commingling of earned fees (which should be in operating) sitting in the trust account. The opposite can also be a problem: withdrawing funds before they’re actually earned or before the client is billed (which violates the rule against taking unearned money). Always bill the client (or otherwise have clear documentation of earning the fee) before transferring fee money to your firm account. Another pitfall is using the trust account as a personal “piggy bank” during cash flow crunches – which is strictly forbidden and often ends in severe discipline. Also, never leave the trust account “on autopilot.” For instance, don’t assume a staffer’s handling it and pay no attention – partners are responsible for supervising how client funds are handled. In Utah, partners can be disciplined for trust accounting lapses of their employees if they failed to put proper controls in place (see Rule 5.1 and 5.3 responsibilities). In short, treat the trust account with the same level of security and attention to detail as you would a client’s personal bank account that you’ve been asked to manage.

- Leverage available resources and training: If you’re unsure about any aspect of trust accounting, take advantage of resources offered by the Utah State Bar and others. The Utah Bar’s Practice Portal and CLE courses often include trust accounting modules. The OPC periodically conducts an Ethics School that covers trust fund accounting and law practice management tips (79 Utah lawyers attended the trust accounting CLE offered by OPC in January 2023, underscoring the demand for guidance). Additionally, the American Bar Association and Utah Bar Foundation publish guidelines and checklists for trust recordkeeping. For example, the ABA provides state-by-state trust account recordkeeping charts, and the Utah Bar Foundation can assist with questions about setting up accounts. Don’t hesitate to seek mentorship or consult a legal accountant if needed – the stakes are too high to risk mistakes. As we’ll discuss next, using purpose-built legal accounting software is another smart way to bolster your compliance.

How LeanLaw and Legal Billing Software Support Trust Compliance

Managing IOLTA funds manually – or trying to jury-rig generic accounting software – can be challenging for a busy small firm. This is where modern legal billing solutions like LeanLaw come in, offering automation and safeguards specifically designed for trust accounting compliance. LeanLaw (a legal billing and accounting platform with deep QuickBooks integration) includes several features that align perfectly with Utah’s trust account requirements and best practices:

- Built-in compliance protocols: LeanLaw’s trust accounting engine was developed based on industry best practices and state bar standards. It essentially enforces proper procedures by design. For example, LeanLaw requires you to designate a trust bank account in the software and assign client funds to specific client matters. This ensures identification and separation of each client’s funds within a single IOLTA account. The software will track trust balances per matter, so you’re automatically keeping that sub-account structure that Utah expects. LeanLaw also prevents common errors like applying trust money to the wrong client or overdrawing a client ledger – the system won’t let you spend more from a client’s trust than they have available.

- Automated three-way reconciliation and real-time visibility: One standout feature is LeanLaw’s ability to maintain a continuous three-way sync between your bank balance, the QuickBooks ledger, and the individual client ledgers in LeanLaw. Because LeanLaw is cloud-based and integrated with QuickBooks Online, every trust transaction entered (whether a deposit or payment) updates across all records. When it’s time to do the monthly reconciliation, much of the work is already done – the totals in LeanLaw should mirror the bank’s balance (once you account for any outstanding items). LeanLaw can generate reconciliation reports and client trust balance reports with a few clicks, greatly simplifying the audit trail. This level of real-time tracking means fewer surprises: you can check the software at any moment to see each client’s exact trust balance and a detailed ledger of activity.

- Streamlined trust fund workflows (deposits & disbursements): LeanLaw takes the headache out of handling money in and out of the trust account. For instance, it enables one-click trust disbursements to pay an invoice from trust funds. Let’s say you’ve completed work and generated a $1,000 invoice for a client who has $1,500 in their retainer. With LeanLaw, applying the trust funds to that invoice is essentially a single step – the software will deduct $1,000 from the client’s trust balance, record the transfer in QuickBooks (from trust liability to income), and note the payment on the invoice. This replaces a complex multi-step process you’d otherwise do manually (writing a trust check, recording a journal entry, etc.), and it ensures accuracy. On the deposit side, LeanLaw also facilitates getting money into the trust account correctly. It can integrate with online payment solutions so that clients’ electronic payments for retainers go straight into the IOLTA account. In LeanLaw, you can easily generate trust deposit links or record e-payments, so you don’t accidentally deposit a retainer into the operating account. By automating these workflows, LeanLaw helps eliminate the human error that often creeps in during manual handling of trust funds.

- Client transparency and communication: LeanLaw’s features not only help the firm internally, but also improve transparency with clients – a factor that goes hand-in-hand with compliance. LeanLaw allows firms to show trust account balances on client invoices or statements, keeping clients informed of their funds on hold. In fact, one law firm administrator noted that after implementing LeanLaw, they include the remaining retainer balance on every invoice, which “lets [the client] know where they stand” and adds peace of mind for both the client and the firm. This practice can prevent disputes by ensuring clients are never in the dark about their money. LeanLaw’s trust reports can also be shared or exported if a client requests a full accounting of their trust funds – a request Utah lawyers must comply with.

- Real-world example – Rust Law: To illustrate how LeanLaw supports trust compliance, consider the case of Rust Law (a pseudonym for a small firm featured in a LeanLaw case study). This firm was struggling with IOLTA management when using a general practice management software (they found retainers were “messed up” and the financial workflow was neglected). They decided to switch to LeanLaw and work with a LeanLaw Accounting Pro (a bookkeeping expert familiar with legal accounting). The result was a complete turnaround: LeanLaw and the accounting expert brought Rust Law’s trust accounting into full ABA compliance, giving the firm peace of mind that retainers were accurate. Because LeanLaw is matter-based in its accounting, it became “much easier to parse” client retainer balances, according to the firm’s administrator, Lisa. Clients now receive invoices that clearly list their trust balance, and the firm experiences no more surprises with trust funds. Lisa observed, “Since I’ve been using LeanLaw, I see the difference: easy access to and accuracy of the retainers… LeanLaw is very user-friendly.” This kind of success story underscores that the right software, coupled with sound procedures, can practically eliminate the risk and stress of trust accounting for a small firm.

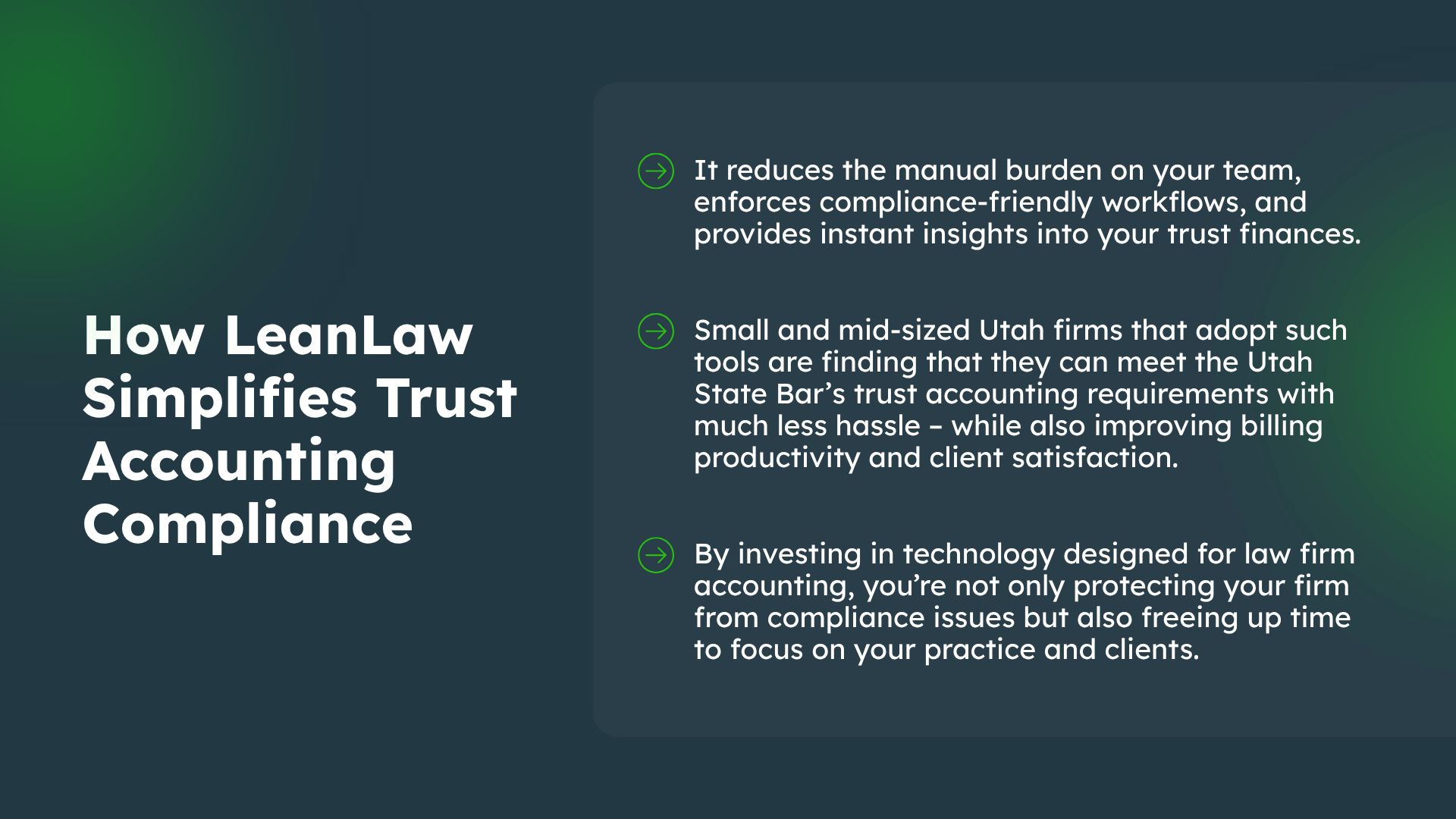

In short, legal-specific billing software like LeanLaw acts as a safety net and efficiency booster for trust accounting. It reduces the manual burden on your team, enforces compliance-friendly workflows, and provides instant insights into your trust finances. Small and mid-sized Utah firms that adopt such tools are finding that they can meet the Utah State Bar’s trust accounting requirements with much less hassle – while also improving billing productivity and client satisfaction. By investing in technology designed for law firm accounting, you’re not only protecting your firm from compliance issues but also freeing up time to focus on your practice and clients.

Internal Resources: To delve deeper into effective trust accounting, check out LeanLaw’s blog articles like the Law Firm Trust Accounting Guide – Best Practices and our Legal Trust Accounting Compliance Checklist. These resources provide additional tips and state-by-state insights to help your firm refine its trust accounting processes.

FAQ: Utah IOLTA and Trust Accounting Compliance

Q: Is an IOLTA trust account mandatory for all Utah attorneys?

A: Yes – if you practice in Utah and handle client funds, you are required to maintain an IOLTA trust account. The Utah Supreme Court’s rules make IOLTA participation mandatory for any attorney who receives client money such as retainers, settlements, or advance fee payments. (If you never handle client funds – e.g. certain government lawyers or in-house counsel – you might be exempt, but most private practice lawyers need an IOLTA.) The account must be set up in a designated trust account at a bank, and you must register it with the Bar. Remember that all interest earned on IOLTA accounts is forwarded to the Utah Bar Foundation to support legal aid, per Rule 14-1001. You do not get to keep interest on client trust funds in Utah.

Q: How do I set up an IOLTA account in Utah and where should I bank?

A: To open an IOLTA, first choose a bank or credit union that is approved by the Utah State Bar. Utah law requires attorneys to hold IOLTA funds at approved financial institutions that meet certain criteria (for example, agreeing to remit interest to the Bar and to notify the OPC of any bounced checks). The Utah Bar Foundation website lists banks that offer IOLTA accounts in Utah. You can often open the IOLTA at the same bank where your firm’s operating account is, as long as it’s an approved institution.

You’ll typically fill out a form provided by the Bar Foundation (often called a “Notice to Financial Institution” form) when you open the account, which the bank will use to set up the account correctly (with the Bar Foundation’s tax ID for the interest). When naming the account, make sure the title clearly indicates it’s a trust account (e.g. “Smith Law PLLC Client Trust Account (IOLTA)”).

This helps avoid any confusion and ensures bank reports are correctly routed. Once open, report the account number to the Bar if required (Utah’s annual license renewal includes an IOLTA certification where you list your trust account). Setting up an IOLTA is straightforward, but managing it properly is the ongoing part – which brings us to compliance.

Q: Do all client funds go into the IOLTA account, or can some be kept separately?

A: Most small or short-term client funds will go into the pooled IOLTA account, but not always all client funds. Utah (like other states) allows attorneys to use a separate interest-bearing trust account for an individual client if the amount is large enough or will be held long enough that the interest could benefit that client. In other words, if holding a very substantial settlement for many months, you should likely set up a dedicated trust account for that client so they (not the Bar Foundation) earn any interest.

On the other hand, if the client funds are nominal in amount or short-term, they belong in your IOLTA. The guiding principle is: you have a fiduciary duty to act in the client’s best interest. If their money can earn net interest for them, put it in a separate account for the client. If not, IOLTA it. In all cases, never put client funds in a non-trust account. It’s either IOLTA or a separate client trust account – never your general business account.

Q: What records do I need to keep for my Utah trust account, and for how long?

A: You should keep detailed records of every transaction in and out of the trust account. This includes: bank statements, deposit slips, canceled checks (or check images), client ledgers showing each client’s balance and activity, a master ledger for the whole account, retainer agreements or other documents authorizing you to hold the funds, and invoices or statements showing how and when funds were disbursed.

Essentially, an auditor should be able to reconstruct the story of each client’s funds from your records. Utah’s rules don’t specify an exact retention period in the text of RPC 1.15, but the common requirement (and best practice) is to retain all trust account records for five years after the termination of the representation or disbursement of the funds. This mirrors the ABA Model Rule and ensures you have documentation in case a question arises later.

In addition to keeping records, you must perform monthly reconciliations and keep a record of those reconciliations. If using software like QuickBooks or LeanLaw, you can save or print the reconciliation reports. By having 5+ years of complete records, you’ll be prepared if the OPC asks for documentation or if you ever need to answer a client’s questions about their money.

Q: How does the Utah Bar find out about trust account problems? Do they audit lawyers?

A: Utah does not currently conduct routine random audits of all trust accounts, but the Bar has proactive monitoring mechanisms. Banks are required to alert the Utah Office of Professional Conduct if a trust account check bounces or is presented against insufficient funds. Even if it’s an innocent overdraft (say you mistimed a deposit), the OPC will get a notice and may follow up with you to investigate what happened.

Additionally, most trust account discipline cases begin with a client complaint – for instance, a client says, “My lawyer won’t return my money” or a successor lawyer reports that funds weren’t properly handled. Once the OPC is alerted, they can demand your trust records and bank statements for review. If they find minor recordkeeping issues, they might caution you or require you to attend a trust accounting CLE.

But serious red flags (e.g. misuse of funds) will lead to a formal ethics complaint. In 2023, the OPC opened 31 new cases just from NSF bank alerts – so even without client complaints, the system is watching. The bottom line is, you should operate as though an audit could happen at any time. Keep your records immaculate and your procedures tight. Many firms even do an internal audit annually (or have their outside accountant do one) to double-check compliance. This way, if the Bar ever comes knocking, you’ll be ready.

Q: What are the potential penalties for trust accounting violations in Utah?

A: The consequences can range from mild to career-ending, depending on the violation’s severity and intent. For minor bookkeeping lapses or isolated mistakes (with no client harm), the OPC might issue a private admonition or a warning, possibly coupled with requiring you to fix the issue or take an education course (Utah often requires an Ethics School focused on trust accounting for such cases).

More serious or repeat violations can result in a public reprimand or probationary period where your trust account is monitored. If client funds were actually misappropriated or misused – even due to negligence – the discipline escalates sharply: suspension of your law license is common for mishandling client money. In the most egregious cases (e.g. theft of client funds or persistent commingling despite warnings), the Utah Supreme Court can order delicensure, which is disbarment.

Along with losing your license, you could be ordered to pay restitution to clients. Keep in mind that even an admonition or reprimand becomes a matter of public record and can damage your reputation. Also, your malpractice insurance may not cover intentional misuse of funds. In short, no financial or personal pressure is worth cutting corners with the trust account – the risk to your professional livelihood is too great.

Q: Can legal software like LeanLaw really help with IOLTA compliance?

A: Absolutely. While software is not a substitute for understanding the rules, the right legal-specific software can significantly reduce human error and streamline compliance. LeanLaw, for example, has features built specifically for trust accounting. It will automatically enforce separation of funds by client, alert you if you try to overdraw a client’s balance, and keep your trust ledgers in sync with your bank and QuickBooks records.

It also makes reconciliation easier by providing one-click reports and even automating parts of the three-way reconciliation process. Many Utah firms use LeanLaw to track retainers, because it will clearly show how much each client has in trust at any moment and it records every deposit and payment with proper descriptions. By using a tool like this, you’re less likely to make math mistakes or bookkeeping omissions that could lead to compliance issues.

Moreover, LeanLaw’s audit-ready reporting means if the OPC ever needs records, you can generate detailed client trust ledgers and reconciliation reports in seconds. In summary, while you still have to follow the rules, software can act as a safeguard – guiding your firm’s trust accounting workflows so that staying compliant becomes much easier and virtually automatic. This allows you to focus on practicing law, confident that the technical aspects of trust management are under control.