Key Takeaways:

- Mandatory IOLTA Participation: Delaware requires lawyers in private practice to keep eligible client funds in Interest on Lawyers’ Trust Accounts (IOLTA), ensuring that interest supports legal aid initiatives. Attorneys must use approved, in-state banks for these trust accounts.

- Strict Trust Accounting Rules: Delaware Lawyers’ Rule 1.15 mandates segregation of client funds, detailed record-keeping for at least five years, and prohibits commingling of client money with firm funds. Monthly reconciliations and careful oversight are critical to avoid ethical violations.

- LeanLaw for Compliance: Legal tech like LeanLaw streamlines trust accounting. LeanLaw’s software automates three-way reconciliation, tracks client ledgers, and integrates with QuickBooks to ensure trust accounting compliance with Delaware’s rules. This helps small and mid-sized firms stay audit-ready and avoid common pitfalls.

Trust accounting is a fundamental responsibility for law firms of all sizes – especially when handling client funds in Delaware. Mismanaging a client trust account can lead to severe disciplinary action or even disbarment. Delaware’s rules are particularly clear: client money is not the lawyer’s money, and it must be safeguarded in special trust accounts separate from the firm’s operating funds. One key component of Delaware trust accounting is the IOLTA program (Interest on Lawyers’ Trust Accounts).

Established in 1983, Delaware’s IOLTA program pools nominal or short-term client funds into interest-bearing trust accounts, with the interest used to fund legal services for those in need. This guide explains what IOLTA is, why it matters, and how Delaware law firms must handle client funds to comply with state bar rules. We’ll also highlight common trust accounting pitfalls (and how to avoid them) and provide tips on setting up workflows for reconciliation and audit readiness – including how LeanLaw’s trust accounting features can help Delaware firms stay compliant.

Why is this important? Beyond ethical duty, compliance with trust accounting rules is critical for your firm’s reputation and license to practice. The Delaware Lawyers’ Rules of Professional Conduct (DLRPC) set strict standards for managing client funds (Rule 1.15 and related provisions), and the Delaware Bar Foundation and Supreme Court enforce rigorous oversight through the IOLTA program and random audits. Even though Delaware has one of the lowest rates of lawyer discipline in the nation, trust account violations are treated very seriously. By mastering Delaware’s IOLTA and trust accounting requirements, your firm can avoid sanctions, protect clients’ interests, and contribute positively to the justice system.

What is IOLTA and Why It Matters

IOLTA (Interest on Lawyers’ Trust Accounts) is a special type of pooled trust account that holds client funds which are small in amount or to be held for a short duration. Instead of each client’s money sitting idle in separate accounts, IOLTA allows lawyers to pool these funds. The interest earned on an IOLTA account is remitted to a charitable fund (in Delaware, the Delaware Bar Foundation) to support legal aid and access-to-justice programs. Importantly, clients do not earn interest on IOLTA-held funds – but they benefit from the legal services infrastructure that the interest helps finance.

In Delaware, participation in the IOLTA program is mandatory for attorneys in private practice who handle client money. This mandatory participation “ensures that all appropriate funds are maintained in IOLTA accounts” and that those accounts earn competitive interest rates for the benefit of legal aid programs. (Delaware’s approved IOLTA banks must offer interest rates comparable to rates paid on similar non-IOLTA accounts.) In practical terms, if you practice law in Delaware and hold client funds, you generally must have an IOLTA trust account.

Why does IOLTA matter? It matters for both ethical and societal reasons:

- Ethical Compliance: Under Delaware Rule 1.15, lawyers have a duty to safeguard client property. IOLTA accounts are a tool for complying with that duty when the client’s funds are too nominal or short-term to justify a separate account. By using IOLTA, you ensure you’re not improperly holding or benefitting from client money – avoiding commingling and keeping client funds separate, as required by professional conduct rules.

- Supporting Legal Aid: On a broader level, IOLTA turns “idle” pennies into funding for civil legal aid. Delaware was an early adopter (since 1983) of IOLTA. Each Delaware law firm’s participation contributes to a pooled fund that the Delaware Bar Foundation grants out to legal services for vulnerable communities. In other words, your compliance helps bridge the justice gap.

How IOLTA Works in Delaware: You deposit qualifying client funds into a pooled trust account designated as “IOLTA.” All Delaware IOLTA accounts must be held at eligible financial institutions – banks or credit unions approved by the Delaware Lawyers’ Fund for Client Protection (LFCP) and the Bar Foundation. Delaware’s rules even require the bank to have a brick-and-mortar presence in the state. These approved banks have signed agreements to: (1) pay the highest available interest rates on IOLTA deposits (so charitable revenues are maximized) and (2) send overdraft notifications to regulators if a trust check bounces.

When you set up an IOLTA account, you must notify the Bar Foundation of your enrollment. The account should be clearly named as a trust account (for example, “Attorney Trust Account (IOLTA) – [Firm Name]”) to avoid any confusion with operating funds. Which funds go into IOLTA? Delaware’s Rule 1.15(f) provides guidance: if the funds are not large enough, or not expected to be held long enough, to earn net interest for the client (after accounting for bank fees and administrative costs), then those funds are “IOLTA-eligible” and must go into the IOLTA account.

For example, a typical retainer of a few thousand dollars that will be used within weeks or months is usually IOLTA-eligible – the interest it could earn individually is negligible, so that interest is better pooled for charity. On the other hand, substantial funds that will be held for a long period should not go into IOLTA: in those cases, the lawyer is expected to set up a separate, interest-bearing trust account for that client so the client can receive the interest. Determining this is part of the lawyer’s fiduciary duty: Will the client’s funds earn income in excess of the costs to manage it? If yes, a separate account is warranted; if no (i.e. the amount or timeframe is too limited), use IOLTA.

In summary, IOLTA is both a compliance mechanism and a community service initiative. Delaware law firms benefit from knowing they are handling client funds correctly and contributing to a good cause. Failing to use an IOLTA when required – such as keeping client money in a non-interest-bearing account or in your own account – isn’t just a missed opportunity for charity, it’s an ethical violation that can put your license at risk.

Delaware’s Trust Accounting Rules and Ethical Obligations

Delaware’s Lawyers’ Rules of Professional Conduct impose strict statutory and ethical obligations on how attorneys must handle client funds. Rule 1.15, titled Safekeeping Property, is the primary rule governing trust accounts. Here are the key requirements Delaware law firms must follow:

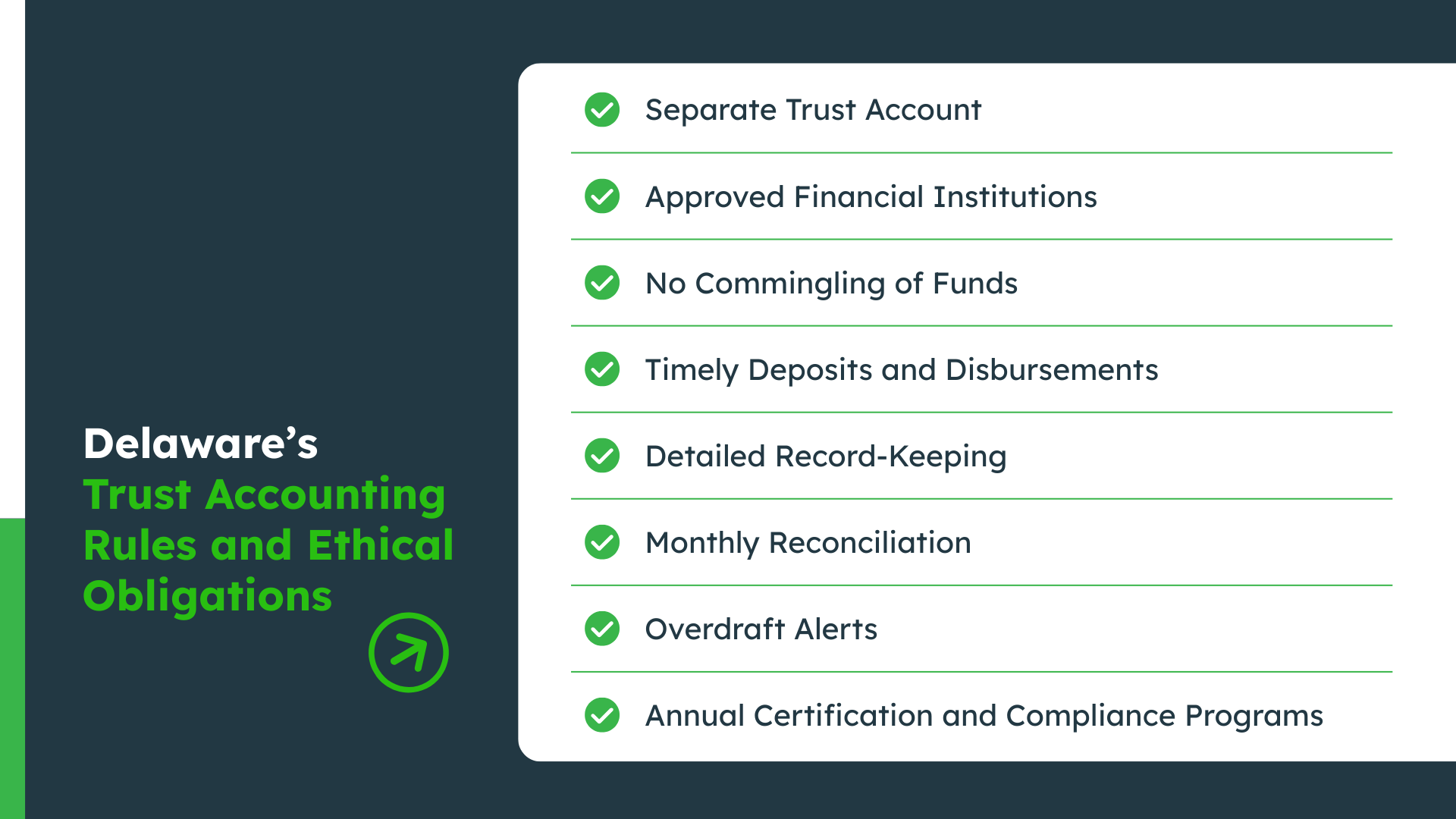

- Separate Trust Account: “Any funds a lawyer holds on behalf of a client or third party must be deposited into a trust or escrow account designated solely for funds held in connection with the practice of law in Delaware.” (Rule 1.15(a)). In practice, this means you cannot deposit client money into your law firm’s operating account or any personal/business account. You need a dedicated trust account (or accounts) for client funds. Most firms maintain one primary pooled trust account (their IOLTA) for all clients, but you may have multiple trust accounts if needed for certain clients or matters. Every such account must be clearly labeled (e.g. “Client Trust Account” or “Escrow Account”) to distinguish it from operating funds.

- Approved Financial Institutions: All attorney trust accounts in Delaware must be held at approved banks. The Delaware Supreme Court (through the Lawyers’ Fund for Client Protection) maintains a list of approved financial institutions that have agreed to meet the IOLTA requirements and report overdrafts. Before opening a trust account, Delaware lawyers should check that the bank is on the approved list. (These are typically banks with a Delaware branch that offer the required interest comparability and oversight agreements.) Using a non-approved bank would violate Rule 1.15A and could jeopardize your compliance status.

- No Commingling of Funds: Lawyers must not commingle client funds with their own funds. This cardinal rule means you cannot use a client trust account to hold your firm’s money, and vice versa. The only exception Delaware (like many jurisdictions) allows is that a lawyer may deposit a small amount of personal funds into the trust account solely to cover bank service charges. In Delaware, Rule 1.15 explicitly permits up to $2,000 of the firm’s funds to be kept in an IOLTA account to pay bank fees if necessary. Aside from that, every penny in the trust account must belong to clients or third parties (e.g. settlement funds, advance fees, escrow deposits) – misuse of client funds or mixing them with firm money is considered misappropriation. Commingling is one of the gravest errors in trust accounting, often leading to discipline.

- Timely Deposits and Disbursements: Delaware lawyers are expected to deposit client funds into the trust account promptly (typically, no later than the next business day after receipt). Likewise, when funds need to be disbursed (e.g. paying a client or a third party from a settlement), that should be done without undue delay once the funds are cleared and authorized. This promptness ensures that client money is always where it’s supposed to be. Rule 1.15 also requires that upon receiving funds or property in which a client has an interest, the lawyer must promptly notify the client and deliver any funds the client is entitled to receive. In practice, develop a habit that every check or payment in goes into the trust account immediately, and any payment out (to or on behalf of the client) is properly documented and executed from the trust account. Never “borrow” from client funds or use one client’s money to pay another client’s liability – these are serious violations.

- Detailed Record-Keeping: Proper trust accounting means meticulous record-keeping. Delaware Rule 1.15(d) lays out record retention requirements: you must maintain complete records of client trust account funds for at least five years after the termination of each representation or the conclusion of the fiduciary obligation. This includes bank statements, cancelled checks, deposit slips, ledgers for each client, and reconciliation reports. In the event of an audit or disciplinary inquiry, you’ll need to produce these records to demonstrate every transaction was handled correctly. Inadequate record-keeping (e.g. missing ledgers or receipts) not only hampers your ability to manage the account but can invite trouble during a compliance audit. Best practice is to use a modern accounting system (or dedicated legal trust accounting software) to keep digital records, while also keeping any required paper records organized. Each client should have their own ledger listing all deposits, disbursements, and current balance. The sum of all client ledger balances should at all times equal the total balance in the trust bank account – if not, something is wrong.

- Monthly Reconciliation: While Delaware’s Rule 1.15 does not explicitly spell out a monthly reconciliation requirement, it is effectively expected as part of proper record-keeping and is considered a best practice nationwide. You should reconcile each trust account every month: comparing the bank statement balance to your internal records and client ledgers, and resolving any discrepancies. Neglecting regular reconciliations is a common pitfall that can allow errors or theft to go unnoticed. Delaware’s Certificate of Compliance (discussed below) essentially forces firms to confirm that they are balancing their books. A monthly three-way reconciliation (bank balance, lawyer’s trust ledger balance, and sum of individual client sub-account balances all matching) is considered the gold standard. If you use software like LeanLaw or QuickBooks with a trust accounting feature, much of this can be automated or at least greatly simplified.

- Overdraft Alerts: Delaware has a robust overdraft notification rule (Rule 1.15A). Every approved bank holding a trust account must agree to notify the Office of Disciplinary Counsel (ODC) if any instrument is presented against insufficient funds in a lawyer’s trust account. This means if you bounce a trust account check (or even if a check would bounce but the bank covers it), the regulators will know. An overdraft on a trust account is a huge red flag; even if it’s an innocent mistake, it will trigger scrutiny. Always ensure there are cleared funds in the account before any disbursement. Pro tip: because client payments (like settlement checks) can take time to clear, never assume a deposit is available until the bank confirms it; and never disburse on uncleared funds. Also, keep that permissible cushion (up to $2,000 of firm funds) in IOLTA if needed to absorb small fees or fluctuations – it can prevent accidental overdrafts due to bank charges.

- Annual Certification and Compliance Programs: Delaware requires lawyers and law firms to annually certify their compliance with Rules 1.15 and 1.15A. In fact, a managing partner (or sole practitioner) must personally review these rules each year and sign an Annual Registration Statement certifying that the firm’s handling of trust accounts is in accord with the rules. The Lawyers’ Fund for Client Protection has developed an “Audit Program” – essentially a detailed checklist of trust accounting compliance items – that firms can use as a self-audit to prepare for certification. Many firms choose to engage an independent CPA to perform a pre-certification audit of their trust accounts, using the Supreme Court’s audit program, and then attach the CPA’s report to their annual certificate. This proactive step can catch any issues early and give both the firm and the court assurance that the books are in order. While not mandatory, it’s a practice worth considering, especially for mid-sized firms with a high volume of trust transactions.

In summary, Delaware’s ethical rules demand vigilance and transparency in all handling of client funds. The combination of mandatory IOLTA participation, strict segregation of funds, detailed records, and oversight mechanisms (like overdraft alerts and compliance certifications) creates a framework where client money should be uniformly safe. For your law firm, this means establishing internal policies that every employee follows when dealing with client money – from the moment a retainer check arrives, to the issuance of a settlement check at case’s end. As we discuss next, many disciplinary cases arise from a few common mistakes. Understanding those pitfalls will help you design your workflows to meet these obligations consistently.

Common Trust Accounting Pitfalls (and How to Avoid Them)

Even well-meaning lawyers can run into trouble with trust accounting if proper systems and attentiveness are lacking. Here are some of the common pitfalls Delaware law firms should watch out for, and tips on how to avoid them:

- Commingling Funds: Mixing client trust funds with the firm’s own money is strictly forbidden and highly dangerous. This can happen inadvertently – for example, depositing a check made out to the law firm into the trust account when it was actually earned fee, or paying a firm bill from the trust account. Avoid it: Maintain separate bank accounts as required, and clearly label them. Use your accounting software to track trust vs. operating funds carefully. Double-check checks and deposit slips – are you using the trust account only for client-related funds? Remember, even “borrowing” client money for a short time is unethical. Delaware’s Rule 1.15 is clear that client funds are off-limits for personal or business use. Train all staff that handle funds on this rule so they don’t accidentally commingle.

- Failure to Reconcile Regularly: Not reconciling your trust account on a monthly basis is asking for trouble. If you’re not comparing the bank statements to your internal records, you might miss errors or theft. Small accounting mistakes (a transposed number, a bank fee you forgot to record, etc.) can snowball. Avoid it: Schedule a dedicated time each month to perform a three-way reconciliation (bank balance vs. general ledger vs. client ledgers). Many firms do this right after the monthly bank statement arrives. Use tools or software that can generate reconciliation reports and highlight discrepancies. If something doesn’t add up, investigate immediately – it’s much easier to fix issues sooner than later. In Delaware, being able to demonstrate a history of monthly reconciliations is part of showing you’re audit-ready.

- Inadequate Record-Keeping: Poor record-keeping – like failing to maintain individual client ledgers, or not keeping copies of deposit slips and disbursement records – can lead to big problems. Without detailed records, you can’t prove compliance in an audit, and you may not realize a shortfall until it’s too late. Avoid it: Use a dedicated trust accounting system or at least a spreadsheet that tracks every transaction. For each client matter, record the date, amount, and purpose of every deposit and withdrawal, and keep a running balance. Preserve all supporting documents (many banks provide images of cancelled checks online – save those, or if using paper checks, keep copies). Delaware requires five-year retention of these records, so set up an organized filing (physical or digital) that you won’t lose. If you ever part ways with a client, you’ll need those records for the required period.

- Improper Withdrawals or Disbursements: Taking money out of the trust account at the wrong time or for the wrong purpose is a serious violation. Examples include withdrawing fees before they are earned (unless the client has given informed consent to treat a retainer as earned on receipt), or paying the wrong client. Avoid it: Only disburse client funds for legitimate, authorized purposes – typically, paying the client, paying a third-party on the client’s behalf (like a medical lien or court fee), or transferring earned fees to the firm (after invoicing the client). Always get client permission where needed and document it. If withdrawing earned fees, invoice the client and make the transfer promptly, with records showing the balance reduction for that client. Never use one client’s funds to cover another client’s payment. Having a good ledger system will prevent you from overdrawing one client’s balance. And of course, never withdraw funds for personal use or before you’re entitled to them – that’s misappropriation.

- Lack of Client Communication: Clients should never be in the dark about their money. If you don’t inform clients about the receipt of their funds or provide accounting when requested, it erodes trust and could result in complaints. Avoid it: Follow Rule 1.15’s mandate to promptly notify clients of received funds and to deliver funds they are entitled to. It’s good practice to send a receipt or confirmation when you deposit a client’s retainer, and to provide regular statements (especially if the funds are held for a long time). If a client asks for a report of their trust balance, be prepared to give a clear, updated accounting. Transparency can prevent misunderstandings – many grievances start because a client “didn’t know where the money went.”

- Insufficient Training and Oversight: In some firms, the attorneys might leave trust accounting to a bookkeeper or office manager without proper training, or a new associate might not know the rules. Mistakes then happen due to lack of knowledge. Avoid it: Ensure that anyone handling the trust account – whether it’s a partner, a paralegal, or an external bookkeeper – is well-versed in Delaware’s trust accounting requirements and the firm’s internal procedures. Consider a training session for new hires on how to process client funds. Additionally, establish internal oversight: for example, have a second person review the reconciliation monthly, or require two signatures for large trust disbursements. The goal is to catch errors and deter misconduct. Staying updated on rule changes is also key (for instance, if Delaware modifies IOLTA rates or procedures, your firm should know).

- Not Adhering to Jurisdiction-Specific Rules: Each state has nuanced differences in trust accounting rules. Delaware has unique aspects (like the $2,000 buffer allowance, the physical presence requirement for banks, and the annual certification). A pitfall for multi-jurisdictional firms or new Delaware attorneys is assuming the rules are the same as elsewhere. Avoid it: Always familiarize yourself with Delaware’s specific rules – read Rule 1.15 and the associated sections 1.15A, etc., as well as any Delaware State Bar or ODC guidance. Failing to follow the exact rules of your jurisdiction can lead to disciplinary action. If you practice in Delaware even part-time (or handle Delaware client funds), those funds must be in a Delaware-compliant trust account. When in doubt, consult the Delaware Bar’s ethics hotline or refer to resources like the Delaware Bar Foundation’s IOLTA FAQ (which we’ve cited here) to ensure you’re meeting all requirements.

By being aware of these common pitfalls and implementing safeguards, your firm can maintain the highest standards of trust accounting. Many of these mistakes are preventable with a combination of diligent procedures and good tools. In the next section, we’ll discuss how leveraging technology – specifically, LeanLaw’s trust accounting features – can help automate and enforce some of these best practices, making compliance easier for small and mid-sized firms.

How LeanLaw’s Trust Accounting Features Help Delaware Firms Stay Compliant

Modern legal accounting software can be a game-changer for managing trust accounts. LeanLaw, for example, offers specialized trust accounting features designed to keep law firms compliant with state bar rules while simplifying the day-to-day work. Here’s how LeanLaw can help Delaware lawyers meet their trust accounting obligations:

- Built-In Compliance Controls: LeanLaw’s trust accounting engine is built around industry and state bar standards. It enforces the separation of funds and tracking required for ethical compliance. For instance, LeanLaw requires you to designate trust deposits to specific client matters and prevents you from applying those funds to anything other than that client’s invoices or authorized disbursements. This structure inherently guards against commingling and accidental misuse of funds.

- Client-by-Client Ledger Tracking: Every deposit or payment in LeanLaw is tied to a client and matter. The software maintains individual client ledgers automatically. At any given moment, you can see exactly how much money you hold for each client, and for what purpose. This makes it easy to answer client inquiries and produce an accounting on demand. It also ensures that when you review your trust account, you’re really reviewing many sub-accounts (one per client) – a key to spotting discrepancies.

- Automated Three-Way Reconciliation: LeanLaw integrates with QuickBooks Online and your bank data to enable continuous three-way reconciliation. In practice, this means your trust account balance in LeanLaw will always sync with the actual bank balance (via QuickBooks) and the total of all client ledger balances. The software flags any inconsistencies. By having this real-time or on-demand reconciliation, you are “audit-ready” at any moment. LeanLaw essentially reduces the monthly reconciliation from a laborious manual chore (which might be a 12-step process in QuickBooks alone) to just a few clicks. Delaware firms can thus quickly generate reconciliation reports to satisfy the annual audit program or an ODC inquiry without pulling out hair.

- IOLTA-Friendly Workflows: LeanLaw is designed with IOLTA accounting in mind. For example, when you receive client money that needs to go into trust, LeanLaw guides you to record it properly as a trust deposit (not income). When it’s time to pay a client’s invoice from the trust account, LeanLaw’s software will transfer the funds from the trust ledger to operating (after you’ve billed the client) in a compliant manner – ensuring that the invoice payment is recorded as coming from trust and reducing the client’s trust balance accordingly. This kind of workflow integration means you’re less likely to make a data entry mistake that could throw your books off. According to LeanLaw, what might otherwise take 10+ steps in generic accounting software can be done in just a couple of clicks inside LeanLaw.

- Transparency and Audit Trails: Every transaction logged in LeanLaw creates an audit trail – you can see who entered it, when, and why. This is very useful if there’s any question later about a trust fund movement. Also, LeanLaw can generate reports that Delaware firms will find handy, such as: a list of all client trust balances, a detailed ledger report for a specific client, or a report of all trust transactions in a period. These reports can be filtered by date, client, matter, etc., for custom views. Having these at your fingertips means responding to an audit or client question is straightforward.

- Compliance with State Rules: LeanLaw’s team has designed the software to meet ethical and legal requirements across jurisdictions. For Delaware users, that means the software supports the nuances like maintaining that $2,000 cushion if needed, or handling IOLTA interest (LeanLaw will not treat interest remittances to the Bar Foundation as client funds, for instance). While you still need to be aware of Delaware-specific rules (no software can magically know all laws), LeanLaw provides guardrails. It won’t let you overdraw a client’s ledger, for example, which helps you avoid the nightmare of a bounced trust check. In short, LeanLaw acts like a compliance assistant, ensuring your daily practice aligns with what Rule 1.15 and the IOLTA regulations expect.

- Efficiency and Peace of Mind: Perhaps one of the biggest benefits is simply time savings and confidence. Managing a trust account manually (or with a basic spreadsheet) can be time-consuming and stressful. LeanLaw automates the recording of transactions, calculates running balances, and can even automate certain transfers. This reduces the human error factor. With LeanLaw, you can quickly run a reconciliation report or client balance report right before submitting your Delaware Annual Registration compliance certificate, to be sure everything lines up. The software essentially does the heavy lifting, so you and your staff can focus on substantive work. As LeanLaw’s materials note, it “generates accurate and detailed records and reports, and ensures compliance with trust accounting regulations.” By integrating trust accounting into your billing workflow, LeanLaw helps your firm stay compliant without reinventing the wheel each month.

For more on how LeanLaw simplifies trust accounting, you can refer to LeanLaw’s own guides like “Trust Accounting 101: Your Essential Guide” and LeanLaw’s Trust Accounting Features page which detail how the software is tailored for trust fund management. Many small and mid-sized firms have found that using LeanLaw or similar legal-specific accounting software drastically cuts down on errors and increases confidence that they are meeting all bar requirements.

By leveraging technology, Delaware firms can create a fail-safe workflow: client funds come in, are recorded and deposited correctly; the software tracks every movement; monthly reconciliations are a breeze; and the risk of the common pitfalls we discussed is greatly minimized. In the next section, we’ll outline an example trust accounting workflow incorporating some best practices (with or without software assistance) to keep your firm prepared for reconciliations and audits.

Workflow Best Practices for Reconciliation and Audit Readiness

Having the right tools is important, but so is having the right process. Delaware law firms should establish a standard trust accounting workflow that ensures nothing falls through the cracks. Below is an example of a workflow with best practices from deposit to reconciliation, which can be followed manually or with the help of software like LeanLaw. Following these steps will keep your trust account accurate, reconciled, and audit-ready at all times:

- Intake of Funds – Proper Receipt: When a client gives you money (retainer check, settlement check, etc.), immediately issue a receipt to the client and designate what the funds are for. For example, mark a retainer as “advance fee for [Client Name] – to be held in trust.” This establishes transparency with the client and creates a paper trail from the start. Pro tip: Use a receipt book or electronic payment record so you have a duplicate of whatever the client gets.

- Deposit to Trust Account: Deposit client funds into your Delaware trust account promptly – ideally the same or next business day. Always use the trust account deposit slips or clearly indicate the trust account in online banking. If you have multiple trust accounts, deposit into the correct one. Never deposit client money into your operating account. For check payments, wait until the funds clear the bank (and any hold period passes) before you consider them available. Record each deposit in your trust ledger system right away, crediting the specific client’s sub-account. In LeanLaw or similar software, you would create a trust deposit entry tied to the client matter at this point.

- Record-Keeping for Each Transaction: Each time money moves in or out of the trust account, make a detailed entry in your records. This should include: date, amount, client name, purpose of the transaction, and the resulting balance for that client. For example, a deposit entry might read, “01/05/2025 – Deposit $5,000 for John Doe (retainer for case #1234) – new balance for John Doe: $5,000.” A disbursement might read, “02/10/2025 – Payment to Dr. Smith $500 from John Doe’s funds for medical records – new balance for John Doe: $4,500.” Good software will handle the balance math for you; if doing it manually, double-check your arithmetic. Keep all supporting documentation: copy of checks, deposit receipts, wire confirmations, etc., filed by client.

- Segregation of Duties (if possible): In a larger firm, it’s wise to separate who handles the physical money and who handles the record-keeping. For instance, one person (or partner) could authorize disbursements, and another person (bookkeeper) records them and reconciles the account. This internal control can prevent fraud and errors. In a solo or very small firm, you might not have extra staff – in that case, be extra disciplined in your process and perhaps have an outside accountant periodically review your trust records for an objective check.

- Monthly Reconciliation Routine: At the end of each month, reconcile the trust account. This involves three things:

- Bank Reconciliation: Compare the trust account bank statement with your own records. Check off each transaction that appears in both. Investigate any checks that haven’t cleared or any bank fees or interest that you haven’t recorded (remember, interest in IOLTA will go to the Bar Foundation; your bank statement will show it, and you should record it as going out to the Bar Foundation, not as client money).

- Client Ledger Reconciliation: Sum up all individual client balances from your ledger. The total of all clients’ funds should equal the adjusted bank balance (bank balance minus any outstanding checks, plus any deposits in transit). If it doesn’t match to the penny, find out why immediately. Common culprits are math errors, recording an item in the wrong client ledger, or bank charges not accounted for. Delaware expects you to be able to account for any differences – so don’t ignore even small discrepancies.

- Review of Individual Balances: Scan through each client’s ledger for reasonableness. Look for any client with a negative balance (which should never happen – it means you over-disbursed their funds, perhaps using money from others). Also look for funds that have been stagnant too long – are you holding money that should be refunded or paid out? This review helps catch mistakes (like a payment recorded to the wrong client, leaving one with negative balance and another with too high a balance).

- Bank Reconciliation: Compare the trust account bank statement with your own records. Check off each transaction that appears in both. Investigate any checks that haven’t cleared or any bank fees or interest that you haven’t recorded (remember, interest in IOLTA will go to the Bar Foundation; your bank statement will show it, and you should record it as going out to the Bar Foundation, not as client money).

- Document the reconciliation. Save a copy of the bank statement, a print-out of your ledger balances, and a worksheet showing that the totals match. This is what an auditor will want to see. With LeanLaw, you can generate a reconciliation report that includes all this information in one go.

- Address Exceptions Immediately: If your reconciliation uncovers any problems – e.g., a missing $100, or an unknown bank fee – investigate at once. It could be as simple as a data entry omission, which you fix and move on. But if it’s something like a real shortage (say a check was mis-deposited to the wrong account or a check bounced), you need to correct it. For a bounced check, you might have to replenish the funds and then seek the money from the client. Remember that an overdraft notice will be sent to ODC for any bounced trust check, so proactive disclosure to the Bar might be wise if the situation is serious. Timely action can often turn a potential ethics issue into a non-issue (or at least a mitigated one).

- Annual Audit Prep: As part of Delaware’s annual compliance, use December or early January to run through the official Audit Program checklist from the Lawyers’ Fund for Client Protection. This checklist will have you verify things like: Do all your trust checks and deposit slips bear “Attorney Trust Account” on them? Are all your accounts in Delaware and at approved institutions? Did you reconcile every month? Are you over the $2,000 firm funds limit? Have all client matters with balances been reviewed? Completing this internal audit prepares you to confidently sign the Certificate of Compliance for the Supreme Court each year. If you find any issues, either fix them or consider reporting them if required – honesty on the compliance certificate is crucial (a false certification can be separate misconduct).

- Leverage Your Software and Support: If you’re using LeanLaw or a similar system, make sure you’re taking advantage of its features: set up alerts for low balances, utilize reports, and reach out to support if you’re unsure how to record a complex transaction. If you’re not using specialized software, at least use QuickBooks or another accounting tool properly – many accounting systems have a reconciliation module; use it monthly. Also, consider consulting with a CPA or bookkeeper who understands law firm accounting for a quarterly check-up. This is especially helpful for small firms that don’t have multiple layers of staff – an external eye can catch something you missed.

By following a consistent workflow like the above, you create a culture of compliance in your firm. You’ll always know the status of your trust accounting, and you’ll be ready if the Delaware Bar Foundation or ODC ever comes knocking for an audit or if a client raises a question. Remember that in trust accounting, attention to detail is everything. It may seem tedious at times, but the cost of a mistake is far greater than the cost of maintaining good habits.

FAQ

Q: What does “IOLTA” stand for, and do I need an IOLTA account in Delaware?

A: IOLTA stands for Interest on Lawyers’ Trust Accounts. It’s a program where lawyers hold client funds that are small in amount or short-term in a pooled, interest-bearing trust account. In Delaware, yes, if you are in private practice and handle client money, you are required to have an IOLTA trust account (unless the funds are significant enough to warrant a separate account for the client). The interest from IOLTA accounts is given to the Delaware Bar Foundation to fund legal aid, not to the clients or lawyers. Essentially, IOLTA is the default trust account for most routine client funds in Delaware.

Q: Who must participate in IOLTA and are there any exceptions?

A: All Delaware attorneys in private practice who hold eligible client funds must participate. Delaware is a mandatory IOLTA state. The only exceptions are for lawyers who never handle qualifying client funds (for example, maybe you only work on a salary and don’t take client money) – those lawyers can certify themselves as exempt on their annual registration. Also, certain government attorneys, in-house counsel, or others not in private practice are exempt. But if you ever come into possession of client or third-party funds in connection with your practice, you need to use an IOLTA or appropriate trust account. Even law firms typically just maintain a firm-wide IOLTA that covers all lawyers in the firm (individual lawyers don’t each need their own separate IOLTA account as long as the firm’s accounts are compliant).

Q: Can I use any bank for my law firm’s trust account?

A: No – Delaware restricts trust accounts to approved financial institutions. The bank must be approved by the Delaware Lawyers’ Fund for Client Protection (the state’s agency that oversees trust compliance). Approved banks have signed agreements to provide IOLTA interest and to report any trust account overdrafts to regulators. They also must have a physical presence in Delaware. You can find the list of approved banks on the Delaware Courts or Bar Foundation website. Before opening a trust account, always confirm the bank is on the approved list. Using a non-approved bank could put you out of compliance with Rule 1.15A(b).

Q: What records am I required to keep for my trust account, and for how long?

A: Delaware requires that you keep complete records of your trust account transactions for at least five years after the end of the year in which the last transaction for that client occurred. These records include bank statements, canceled checks, deposit slips, client ledgers, check registers, reconciliations, and any other documentation of transactions. It’s wise to keep these organized by year and client. Also, if your trust account is audited or if a question arises, you should be able to produce those records. In practice, many firms keep records even longer (digital storage makes this easier) in case issues surface later. Remember that ethical rule: you must be able to account for every penny of client money. Good record-keeping is your proof.

Q: How often should I reconcile my trust account, and what does a “three-way reconciliation” mean?

A: You should reconcile your trust account every month at minimum. In fact, many firms do it continuously or bi-weekly, but monthly is the standard because you get a bank statement each month. A three-way reconciliation means you are comparing three sets of figures: (1) the bank statement balance for the trust account, (2) your internal trust account ledger balance (checkbook balance), and (3) the sum of all your individual client ledger balances. All three should be identical (after accounting for any in-transit items like outstanding checks). If they’re not, something is off – either a data entry error, a bank error, or worse. Delaware’s regulators strongly expect lawyers to perform this three-way reconciliation regularly as part of maintaining proper records (this is built into many states’ rules and is considered a best practice nationwide). Performing monthly reconciliations is also essential for your annual compliance certification where you affirm that your trust account is balanced and maintained properly.

Q: What are some quick tips to avoid trust accounting mistakes?

A: The biggest tips are: never commingle funds, always track every transaction (no matter how small), and reconcile often. Specifically:

- Deposit client money into trust immediately and don’t leave it lying around (un-deposited checks can be forgotten or misplaced, which is a compliance issue).

- Don’t pay anything out of trust that isn’t related to the client who owns the funds, and don’t pay yourself from trust until fees are earned and invoiced.

- Use detailed memo lines on checks and accounting entries so it’s clear what each payment is for.

- If you’re ever unsure, ask – Delaware’s Office of Disciplinary Counsel or Bar Association can provide guidance on ethical questions. It’s better to take a minute to confirm than to do something wrong.

- Consider using legal-specific accounting software (like LeanLaw or others) – they are designed to prevent many of the common errors by structure. LeanLaw, for instance, won’t let you overdraft a client’s account in the system, and it automates record-keeping tasks.

- Finally, cultivate a mentality that the trust account is sacred. Treat every client dollar as something you must account for. That mindset will naturally lead you to be careful and methodical, which is exactly what trust accounting demands.

Q: How can LeanLaw or similar software actually help my Delaware firm stay compliant?

A: LeanLaw is designed with features that directly address compliance needs. For example, LeanLaw provides a built-in three-way reconciliation tool that keeps your trust balance aligned with your QuickBooks ledger and bank balance in real time. It automates trust transactions – when you receive a payment, you enter it once and LeanLaw logs it in the client’s trust ledger and syncs with QuickBooks. It also prevents common errors: you can’t accidentally use one client’s funds for another, because the software tracks balances per client. It generates reports that you can use for Delaware’s compliance (like listing all client balances at year-end, or showing all activity over a period). Basically, LeanLaw handles the heavy lifting of record-keeping and calculations, so you can focus on reviewing the reports for accuracy. It’s like having an assistant who is expert in trust accounting. Many small and mid-sized firms in Delaware find that this not only saves time but gives peace of mind – you know that if an auditor asked for records or if you need to fill out the annual certificate, you can easily pull the data you need, confident that it’s up-to-date and correct. And because LeanLaw integrates with banking (through QuickBooks Online), it helps catch any discrepancies quickly. In short, while you still need to understand the rules, software like LeanLaw ensures your everyday practice automatically aligns with those rules, drastically reducing the chance of an oversight.

Q: What happens if a Delaware lawyer mishandles client trust funds?

A: Failing to follow trust accounting rules can lead to serious consequences. The Office of Disciplinary Counsel investigates trust account irregularities and can bring disciplinary actions. Outcomes range from admonitions or mandatory training for minor record-keeping lapses, up to suspension or disbarment for severe violations (especially misappropriation of client funds). In some cases, if a lawyer intentionally steals client money, criminal charges for theft or embezzlement can apply – the Delaware Supreme Court has not hesitated to disbar attorneys for trust account abuse. Even unintentional mistakes can result in sanctions if client funds were put at risk. Additionally, the Lawyers’ Fund for Client Protection may pay claims to clients who lost money, and then they will seek reimbursement from the attorney. In short, the professional and personal risk is immense. The best way to avoid discipline is to diligently follow the rules we’ve discussed: segregate funds, keep good records, reconcile, and never “borrow” from the trust. If you realize you made a mistake (for example, you discover a trust accounting shortage), it’s often wise to self-report and correct it, as proactive honesty can mitigate the disciplinary outcome. However, with careful adherence to Delaware’s requirements and using available tools, you can steer clear of these dangers altogether.

By understanding and implementing Delaware’s IOLTA and trust accounting requirements, small and mid-sized law firms can protect their clients’ funds and their own reputations. The rules may seem strict, but they boil down to a simple principle: it’s the client’s money, not yours, until you’ve earned it or disbursed it properly. Through mandatory IOLTA accounts, detailed record-keeping, and prudent workflows (aided by software like LeanLaw for efficiency), Delaware attorneys can fulfill their fiduciary duties with confidence.

Trust accounting done right not only keeps you compliant and audit-ready – it also reinforces client trust in your firm, showing that you run a professional and ethical practice. Compliance is not just a legal obligation, but a cornerstone of good service. With the guidance in this article, your firm should be well on its way to mastering trust accounting in the First State. Safe handling of client funds is a win-win: clients are protected, your firm stays out of trouble, and you contribute to the greater good through the IOLTA program. Happy (and compliant) accounting!