Trust accounting is often cited as one of the biggest headaches for small and mid-sized law firms. Attorneys may feel that managing an IOLTA account is like navigating a “complex maze” – one wrong turn could put their license at risk. In New Jersey, these challenges are amplified by strict state-specific rules and active enforcement.

Law firm leaders already juggling client work and firm management can find it overwhelming to track every penny of client funds, perform detailed reconciliations, and keep up with evolving regulations. Yet trust account compliance is not optional – it’s an ethical and legal obligation. Mismanaging client funds, even inadvertently, can lead to hefty fines, damaged reputation, or even disbarment.

The good news is that with the right knowledge, systems, and tools, New Jersey attorneys can master IOLTA and trust accounting compliance. This guide will break down the essentials of IOLTA, New Jersey’s unique requirements, and best practices to help your small or mid-sized firm stay on the right side of ethics rules and keep client funds safe.

What Is IOLTA and Why New Jersey Requires It

IOLTA stands for Interest on Lawyers’ Trust Accounts. It’s a special type of trust account that attorneys must use to hold client funds that are small in amount or to be held for a short duration. Rather than those funds sitting idle, the IOLTA program pools them and uses the interest to support public interest causes. New Jersey established its IOLTA Fund in 1988 (originally as an optional program) to fund civil legal services for the poor and other justice-related programs. Since 1993, participation in IOLTA has been mandatory for attorneys in private practice. This means if you practice law in New Jersey and handle client money, you are required to have an IOLTA trust account.

The basic concept is straightforward: client funds that cannot practically earn net interest for the client (because the amounts are too small or will be held too briefly) must go into an IOLTA account. For example, a typical retainer or settlement proceeds awaiting disbursement would be deposited in your IOLTA. The bank forwards any interest earned on that account to the state’s IOLTA Fund automatically. (By rule of thumb, if the funds would earn less than about $150 in interest, they belong in IOLTA.)

On the other hand, if you’re holding a very large sum for a long period, you should consider setting up a separate interest-bearing trust account for that particular client so the client can receive the interest directly. Ultimately, using an IOLTA versus a separate interest-bearing account is left to the attorney’s good-faith judgment under New Jersey’s guidelines.

Where does the interest money go? In New Jersey, IOLTA funds are a critical source of funding for legal aid and justice initiatives. By court rule, after administrative expenses, 75% of IOLTA revenues go to Legal Services of New Jersey (and its local affiliates) to provide civil legal aid to low-income residents. Another 12.5% is allocated to the New Jersey State Bar Foundation for law-related education, and the remainder is granted to other programs that improve the administration of justice.

Importantly, none of the interest from IOLTA accounts is kept by lawyers or clients – there are no tax consequences to either, and the IRS does not consider IOLTA interest as taxable to clients or attorneys. In short, IOLTA transforms the “pennies” of interest from many small client balances into funding for the public good, all while ensuring lawyers do not benefit personally from holding client money.

Whose Money Goes in the Trust Account?

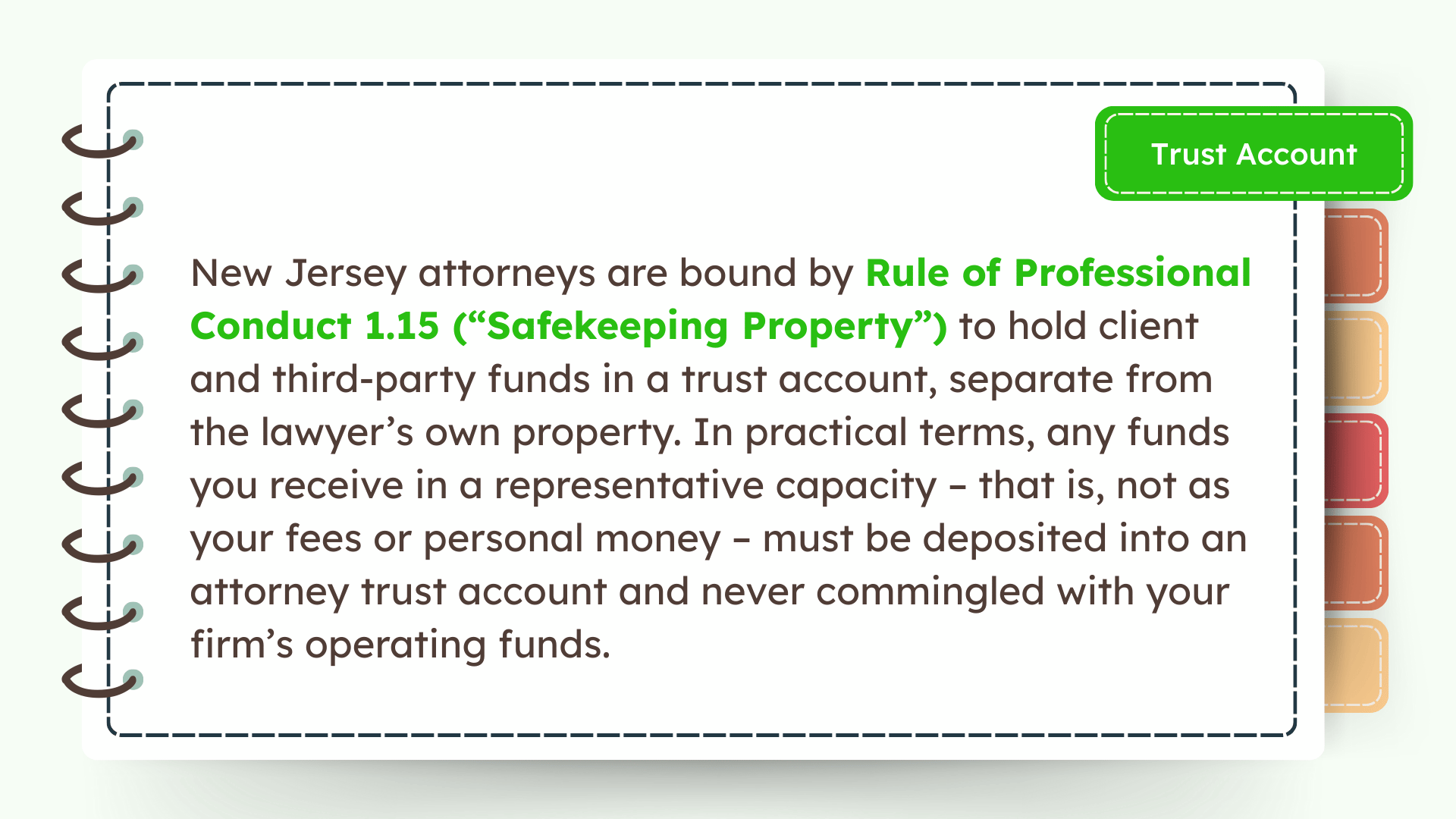

New Jersey attorneys are bound by Rule of Professional Conduct 1.15 (“Safekeeping Property”) to hold client and third-party funds in a trust account, separate from the lawyer’s own property. In practical terms, any funds you receive in a representative capacity – that is, not as your fees or personal money – must be deposited into an attorney trust account and never commingled with your firm’s operating funds.

This includes client retainers or advance fee deposits, settlement proceeds, escrowed funds for a transaction, and any other money you are holding for someone else’s benefit. New Jersey’s court rules explicitly require every practicing attorney to maintain at least two bank accounts: (1) an attorney trust account (commonly an IOLTA account) for client funds, and (2) an attorney business account for the firm’s own funds.

The trust account must be separate from any personal or business accounts and clearly labeled “Attorney Trust Account” on all records, checks, and deposit slips. Likewise, your firm operating account should be labeled “Attorney Business Account” or similar to distinguish it. This clear separation is not just formalism – it’s intended to prevent even accidental use of client money for firm expenses.

What funds go into the trust account? In New Jersey, all funds entrusted to your care in connection with legal representation belong in the trust account until it’s time to pay them out. For example, when a client gives you a $5,000 retainer against future hourly work, those funds are not yours yet – they must be deposited in trust and stay there until you actually earn the fee by completing the work and billing the client.

If you receive a settlement check on behalf of a client, it goes into trust, and you should only disburse it (to the client, to lienholders, and to your firm for fees) as authorized. New Jersey’s RPC 1.15 and related court rules also cover third-party interests in funds. If part of the money may belong to a third party (for instance, a medical provider has a lien, or two clients dispute their shares), you must hold the funds in trust until the dispute is resolved – you cannot simply give all the money to the client or take your fee while ignoring a known third-party claim.

An ethics opinion issued by the NJ Supreme Court’s Advisory Committee on Professional Ethics confirms that lawyers have a duty under RPC 1.15 to honor valid liens or agreements (such as medical liens) and must not disburse disputed funds without resolution.

What doesn’t belong in trust? Generally, your trust account should contain only client or third-party funds – nothing else. It is ethically prohibited to deposit your own money into the client trust account, except for a very limited amount to cover bank service charges. New Jersey permits an attorney to keep a small cushion of personal funds in trust for bank fees – but no more than $250 of the attorney’s own money. Anything above that is considered commingling, which is a serious violation.

For instance, you should never use the trust account to pay your firm’s rent or salaries, nor to hold personal funds or operating capital. Likewise, once client funds are earned or no longer needed in trust, they should be promptly removed from the trust account. If you conclude a matter and a portion of the trust balance is your earned fee, you must transfer that fee to your business account without undue delay. Failing to do so means you’d be leaving your own money commingled in the trust account. Similarly, if you’re holding funds in trust and the purpose for holding them ends (say, a settlement is finalized and all contingencies are resolved), the money should be disbursed to the rightful party – you shouldn’t use the trust account as a storage place for funds indefinitely.

New Jersey ethics regulators often find issues where attorneys leave funds in trust longer than necessary, effectively commingling by inaction. The takeaway is: treat the trust account as sacrosanct for client money only. Put all client-related funds in, keep your own funds out (beyond the token amount for fees), and when in doubt, err on the side of segregating funds in trust until you’re certain they’re earned or properly payable.

New Jersey’s Trust Account Regulations and Recordkeeping Rules

New Jersey has some of the most detailed trust accounting rules in the country, set out in the Court Rules (particularly Rule 1:21-6) as well as the Rules of Professional Conduct (RPC 1.15). Every attorney practicing in NJ must adhere to these requirements – no exceptions for solo or small firms. Below are key aspects of New Jersey’s trust account regulations that small and mid-sized firms need to know:

Approved financial institutions and account setup: Your trust account must be maintained at a bank in New Jersey that has been approved by the Supreme Court of NJ for attorney trust accounts. To get approved, banks agree to certain conditions – most critically, they agree to report any trust account overdraft or bounced check to the Office of Attorney Ethics (OAE). (This is the Trust Account Overdraft Notification Program, an enforcement safety net we’ll discuss later.)

The Supreme Court publishes a list of approved trust account banks each year, and the IOLTA Fund maintains an online list as well. When opening a trust account, ensure the bank knows it’s an attorney trust/IOLTA account; by rule, the account title must include the words “Attorney Trust Account” and for IOLTA accounts, the IOLTA Fund will direct the bank to convert it to interest-bearing status after setup. Many firms also choose checkbooks with a distinct color or design for the trust account to avoid confusion with business checks.

Remember that only a licensed attorney can be an authorized signer on the trust account – you cannot delegate trust check signing to a paralegal or office manager, and even signature stamps are not allowed. This ensures a lawyer is always accountable for any withdrawal. Additionally, the trust account should be used only for client funds related to legal matters. If you happen to wear other fiduciary hats (e.g. serving as executor of an estate or trustee of a family trust), those funds belong in separate fiduciary accounts, not in your attorney IOLTA.

Comprehensive recordkeeping: New Jersey requires “robust” recordkeeping for trust accounts. In practice, this means you must maintain several types of records, including:

- A receipt and disbursement journal (check register) for the trust account, recording every deposit and withdrawal with the date, amount, client matter, and purpose.

- A client ledger for each client or matter whose funds you hold. Each ledger tracks all transactions for that client and shows the current balance of that client’s funds in trust. For example, if you have five clients with money in trust, you should have five separate ledger subaccounts, so you always know exactly how much belongs to each client. It’s critical to update these ledgers with every transaction and keep a running balance; a ledger that isn’t up-to-date defeats its purpose.

- A ledger for nominal attorney funds (the up-to-$250 for bank fees, if you keep such funds in the account). This keeps your bank fee buffer accounted for, so it’s clear that money is not client funds.

- Trust account bank statements and canceled check images. By rule, you must retain copies of all bank statements and either original canceled checks or printed images of canceled checks (with no more than two images per page for clarity). Every trust check and deposit slip should be labeled with the client matter. New Jersey also disallows certain instruments – for instance, do not make trust checks payable to “Cash,” and do not withdraw cash from a trust ATM or teller; all disbursements should be by check or electronic transfer to specified payees for a clear paper trail.

- Accounting of funds disbursed to the attorney. If you pay yourself from trust (for earned fees), the records should reflect the details of that transfer as well (from which client matter, how much, when, and reference to the invoice or fees earned).

These records must be maintained for a substantial period (commonly seven years from final disbursement, per many state rules – New Jersey’s rule also calls for retention of records for seven years from the date of the last transaction, ensuring that in any audit or dispute you can produce the documentation).

The bottom line is that your bookkeeping should be thorough enough that at any given moment you can prove: whose money is in your trust account, how much for each person, and where any money went. If your records are messy or incomplete, you’re inviting trouble.

Monthly three-way reconciliation: A signature feature of New Jersey’s trust accounting compliance is the requirement of monthly reconciliation of the trust account. This isn’t a simple checkbook reconciliation that any business might do – it is a “three-way” reconciliation that is far more rigorous. Each month, you need to verify that three balances match exactly: (1) the bank statement balance for the trust account (adjusted for any outstanding checks or deposits), (2) the total of your trust checkbook or cash journal balance, and (3) the sum of all client ledger balances.

In other words, when you add up the separate balances of every client’s sub-account (plus any $0-250 attorney funds ledger), that total must equal the exact balance in the bank. New Jersey’s recordkeeping rule explicitly mandates having supporting documents each month to show that you performed this three-way reconciliation of the cash journals, checkbook, bank statement, and client ledgers. If there is any discrepancy – even a few dollars – it means something is off that you must investigate and correct immediately.

For example, a common deficiency is when the bank balance doesn’t match the ledger because the attorney failed to record a bank charge or made an arithmetic error. Another red flag is if the total of client balances doesn’t equal the bank balance, which could mean you’ve over-disbursed from one client’s funds by using money belonging to another (a serious problem). A proper three-way reconciliation will catch issues like mathematical errors, bank fees not accounted for, or worse, funds used for the wrong client matter.

Regulators consider three-way reconciliation so important that failing to do it (or to do it properly) is one of the most frequent violations found in random audits. In fact, the very first item on the Office of Attorney Ethics’ common deficiencies list is trust records and bank statements not matching because monthly reconciliations weren’t done or were done incorrectly. The take-away: mark your calendar and reconcile your trust account every single month. Not quarterly, not “when you have time” – monthly without fail.

Finally, keep in mind that New Jersey’s rules make the attorney personally responsible for trust accounting compliance. You can certainly use a bookkeeper or an outside accountant to help manage the records, and many firms do. But you cannot delegate away your ultimate duty to review and ensure accuracy. If you hire an accountant to do monthly reconciliations, the OAE expects that you are also looking at those reports and verifying them. If your software or staff makes an error, it’s still your ethical responsibility to catch and correct it. In a disciplinary audit, claiming “my software messed up” or “my bookkeeper handled that” is not a defense – at best, it might be a slight mitigating factor. The public policy in New Jersey is that attorneys must actively maintain and supervise their trust records in compliance with Rule 1:21-6. This means as a law firm owner or attorney in charge, you should regularly review your trust accounting reports, initial or sign off on reconciliations, and generally know at all times what’s happening with client funds.

The Importance of Three-Way Reconciliation (and How to Do It Right)

It’s worth delving a bit deeper into three-way reconciliation, since this is the linchpin of trust accounting compliance and often the most technically challenging part for lawyers. A three-way reconciliation compares:

- Bank balance – the closing balance on your trust account’s bank statement (after factoring in any checks that haven’t cleared or deposits in transit).

- Book balance – the balance according to your own records (your trust checkbook or running total in your accounting software).

- Client balance – the aggregate total of all individual client ledgers (plus any attorney funds ledger).

For the trust account to be in balance, all three of these numbers must be identical. If they aren’t, something is amiss. For example, suppose your bank statement at June 30 shows $100,000. Your internal trust checkbook also shows $100,000. But when you add up your five client ledgers, you get $98,000 – a $2,000 difference.

That $2,000 discrepancy could be an error (perhaps a deposit was posted to the bank but not recorded on a client ledger, or a math mistake), or it could indicate a misuse of funds (maybe one client’s funds were used to pay another client’s bills inadvertently). The reconciliation process will force you to identify and resolve that issue.

Maybe you find a $2,000 bank service charge that you forgot to record (in which case you need to add $2,000 of firm funds to replenish the shortfall and adjust your books). Or maybe you realize a disbursement was logged under the wrong client’s ledger, making one too low and another too high. By combing through the records to make the balances match, you can catch and correct errors early.

New Jersey requires you to document your reconciliations. In practice, this could be a worksheet or report each month that lists the three balances and shows their agreement (or any adjustments made to get them in agreement). It’s wise to keep a printed copy or PDF of each month’s reconciliation with your trust records. Not only is this required, but it will also impress an auditor and protect you if there’s ever a question.

Many attorneys use software tools or spreadsheets for this. In fact, modern legal accounting software can make reconciliation much easier by automatically updating ledgers and even generating three-way reconciliation reports. For instance, LeanLaw’s trust accounting software is designed to maintain real-time client ledgers and can produce a three-way reconciliation report that compares your QuickBooks balances with bank data to ensure everything is in sync. Even with such tools, though, you should review the reconciliation report each month, sign or date it, and file it.

One more tip: don’t just reconcile the totals – also review each client’s ledger balance periodically. New Jersey auditors have noted that sometimes a three-way reconciliation can technically balance even though there’s a problem, for example if one client’s ledger is negative and another’s is equivalently positive (they cancel out in the total, but that means you’ve used one client’s money to cover another’s).

A proper reconciliation process will include ensuring no individual client ledger is in the red and investigating any that are unusually low or unchanged for long periods. By diligently reconciling and reviewing, you’re not only complying with the rules – you’re protecting your clients and yourself by catching mistakes or misappropriations before they snowball.

Consequences of Non-Compliance: Audits, Discipline, and More

New Jersey takes trust accounting compliance extremely seriously, and the enforcement mechanisms reflect that. Small firms should not assume they’ll fly under the radar. In fact, every law firm, regardless of size, has an equal chance of being audited under New Jersey’s Random Audit Program. The Supreme Court of New Jersey, through the Office of Attorney Ethics (OAE), runs a Random Audit Compliance Program that conducts unannounced audits of law firms’ trust and business accounts.

Each year, a random selection of firms get a letter informing them that an auditor will examine their books and records (typically with about 10 days’ notice). If your number comes up, you’ll need to produce your reconciliations, client ledgers, canceled checks, and other records to show you’re in compliance. The goals of this program are education, deterrence, and detection, according to the OAE. Knowing that you could be audited at any time is meant to deter sloppy practices and prevent the temptation to “borrow” from client funds.

The Random Audit Program has uncovered many instances of deficient practices – and in some cases, actual misappropriation of client money. The OAE reports that in 2023 alone, 769 random audits were conducted statewide. As a result of those audits, 12 lawyers faced disciplinary action, including 3 disbarments, for trust account violations that were detected. These were issues that the lawyers might have otherwise gotten away with, but the random audit brought them to light.

Common problems found include the ones we’ve discussed: failure to do monthly reconciliations, use of client funds for improper purposes, commingling, and poor recordkeeping. If an audit finds minor recordkeeping deficiencies (say, missing labels on checks or a one-time late deposit), the OAE may simply require corrective action. But more significant problems can lead to a formal ethics grievance and charges.

Separately from random audits, New Jersey also has the Trust Account Overdraft Notification Program, which is effectively an automated enforcement trigger. If you or your bank ever bounce a trust account check or if the account is overdrawn, the bank must inform the OAE. This typically prompts an immediate demand from the OAE for an explanation and your trust records. Even if the overdraft was an innocent mistake (e.g., you wrote a check thinking a deposit had cleared, but it hadn’t yet), it will be scrutinized.

In 2023, New Jersey banks reported 143 trust account overdrafts to the OAE. Those led to investigations and ultimately discipline for 8 attorneys (including 1 disbarment) that year. The prior year saw a similar number of overdraft reports (132 in 2022) and resultant disciplinary actions. The lesson here is clear: even a momentary misstep like a bounced trust check can put your license in jeopardy.

Always ensure funds are fully cleared and available before you write a trust check, and double-check you haven’t exceeded a client’s balance. If a mistake happens, be prepared to demonstrate to OAE that it was isolated and promptly corrected – but also expect consequences ranging from a formal reprimand to worse, depending on what they find.

The range of disciplinary consequences for trust accounting violations in New Jersey can be severe. New Jersey is known for a strict stance: the NJ Supreme Court has long held that knowing misappropriation of client funds results in automatic disbarment – permanent loss of license – except in the most extraordinary circumstances. Even lesser infractions can lead to sanctions.

For example, attorneys have been admonished or reprimanded for things like commingling funds or sloppy recordkeeping that doesn’t result in client harm, and censured or suspended for more serious issues like gross neglect of the trust account or negligent misappropriation. The disciplinary reports are full of cases where a lawyer with an otherwise clean record faces public discipline because they didn’t keep the required records or allowed a trust imbalance to occur.

The court’s priority is protecting the public, so intent matters little if client funds were put at risk. In one recent public case, an attorney was reprimanded after an overdraft investigation revealed repeated failure to reconcile and a shortfall in the trust account (even though it was caused by oversight, not theft). On the other hand, any hint that an attorney intentionally used client money for personal purposes (even “just borrowing it” to cover a bill) is likely career-ending in New Jersey.

The OAE has noted that when it detects lawyer theft, it very often results in automatic disbarment – New Jersey is one of the few states that disbars on a first offense for knowing misappropriation, and disbarment in New Jersey is permanent (you cannot apply for reinstatement).

Beyond professional discipline, consider that mishandling client funds can lead to civil liability and even criminal charges in egregious cases. Clients who lose money may sue for malpractice or breach of fiduciary duty. The New Jersey Lawyers’ Fund for Client Protection (a fund financed by attorney annual fees, separate from IOLTA) reimburses clients who are victims of attorney theft, but the Fund will pursue the disbarred attorney for reimbursement and law enforcement can get involved if actual fraud is at play.

While such extreme outcomes usually stem from intentional wrongdoing, even technical violations harm your reputation. No lawyer wants to be in the headlines or explained to clients why their trust account was audited or why there’s an ethics proceeding. In short, the costs of non-compliance – whether measured in stress, time, money, or loss of license – far outweigh the effort needed to stay compliant.

Best Practices for Trust Accounting Compliance in New Jersey

Given the high stakes, what can a small or mid-sized law firm do to ensure smooth IOLTA and trust accounting compliance? Here are some best practices tailored for New Jersey’s rules and a busy law practice:

1. Treat trust accounting as a priority, not an afterthought

It’s easy to procrastinate on bookkeeping when you’re focused on client work. But build habits and internal controls to give your trust account the regular attention it requires. For example, schedule a dedicated time at least monthly (if not weekly) to update trust records and perform the reconciliation. Many successful small firms designate one day early each month for trust accounting catch-up and reconciliation. Consistency is key.

2. Know and follow the rules

Ensure you and your staff are familiar with RPC 1.15 and Rule 1:21-6. Keep a checklist of New Jersey’s requirements handy – e.g. “All trust checks labeled; no cash withdrawals; deposit slips have client matter noted; ledgers updated; monthly reconciliation done,” etc. The Office of Attorney Ethics provides an outline of recordkeeping requirements, and the New Jersey State Bar Association often offers CLE courses or publications on trust accounting compliance. Make use of those resources to stay current. When rules change or new ethics opinions are published, discuss them in the firm and update your practices accordingly.

3. Segregate funds and avoid commingling scrupulously

Always deposit client monies into trust promptly – ideally the same day or next business day after receipt. New Jersey expects “funds shall be deposited in trust as soon as practicable,” and letting checks sit on your desk for a week could be viewed as failing to safeguard client property. Likewise, when it’s time to pay out funds, do so without unnecessary delay.

If a matter concludes and there are unused client funds, return them to the client (or if the client cannot be found, follow the unclaimed property procedures under R.1:21-6(j) or applicable law to remit the funds appropriately). Don’t leave small balances languishing in trust for months or years – that’s a recipe for confusion and possible ethics questions down the road. And as emphasized before, never dip into client funds to cover your own expenses, and don’t deposit your funds in trust (beyond the <$250 for bank fees) even if you think it might “cover” a potential shortfall. The best practice is to run the trust account as if every dollar is untouchable until proper documentation and authorization exist to disburse it.

4. Maintain detailed documentation

Each time you receive money that goes into trust, give the client a receipt or written acknowledgment of the deposit, and keep a copy for your records. Each trust check or payment you issue should likewise be documented with an invoice, settlement statement, or written instructions authorizing that disbursement.

These documents will support the entries in your ledgers and journals. For every transaction, make sure your records answer the vital questions: whose money, what for, how much, when, and to whom paid. During a compliance audit, being able to pull a file and show, for example, a signed settlement distribution sheet that matches the trust disbursements, goes a long way toward demonstrating your professionalism and good faith.

5. Reconcile regularly and review your work

We’ve already underscored the importance of monthly three-way reconciliation, but the best practice is to reconcile as frequently as you can manage – even more often than monthly if feasible. With online banking and modern software, some firms reconcile weekly or even daily in busy times. The more frequently you verify the trust account, the sooner you’ll catch any error. After reconciling, take a moment to scan the client ledger balances.

Ask yourself: Does every active client have the appropriate amount in trust? Is anyone’s balance negative or oddly high? Investigate anomalies right away. Also, if you have others helping with bookkeeping, implement a review system. For instance, the bookkeeper prepares the reconciliation, and then you (the attorney) review and sign off. This dual control is an internal audit that can catch mistakes and also demonstrates that you are supervising, as the rules require.

6. Leverage legal-specific accounting software

Managing trust accounting by hand or in a general business accounting program can be prone to error. Today there are affordable legal tech tools that make trust compliance much easier for small firms. For example, LeanLaw’s trust accounting features integrate with QuickBooks Online to automatically track client trust balances and separate them from operating funds.

With the right software, every time you receive or disburse trust money, you can assign it to a client matter, and the system updates the client ledger and trust account register simultaneously. Modern legal accounting software can also generate reconciliation reports, flag duplicate check numbers, prevent common errors (like accidentally entering a trust check as an operating expense), and even produce alerts if a ledger would go negative.

LeanLaw, in particular, emphasizes identification, separation, and accounting as core pillars: it helps assign each transaction to the right client, keeps those funds completely separate from your business books, and maintains a continuous ledger and audit trail. By using such tools, small firms gain an extra layer of protection – the software acts as a watchdog that aligns with state bar compliance standards. Of course, you still must review and oversee the books, but having automation for the tedious parts can reduce human error and save you countless hours. The investment in a legal-specific accounting solution is often far cheaper than the cost of an accounting mishap or ethics investigation down the line.

7. Implement internal controls and separation of duties

In a larger firm, different people might handle billing, deposits, and reconciliation. In a small firm, one person might do it all – which can be risky if that person (attorney or staff) makes a mistake or, worst case, does something dishonest. Wherever possible, segregate duties: for instance, if you have a bookkeeper recording transactions, have a different person (like yourself or another attorney) review bank statements and canceled checks.

Even within a solo practice, you can create a checklist for yourself to double-check transactions. Always review the actual bank statements each month – don’t just trust a report – to ensure no unknown withdrawals or corrections appear. New Jersey’s system of requiring an attorney signature on trust checks and prohibiting non-lawyer disbursing helps here, but internal vigilance is important too.

If an employee helps with deposits, make sure you still verify those deposits were made. Consider requiring two signatures for any large trust check (if your bank supports that). These kinds of controls are commonplace in business and are equally applicable to law firms to prevent and detect errors or fraud.

8. Be prepared for audits and embrace a compliance mindset

A wise practice is to self-audit your trust records periodically. Perhaps once a year (or more often), pretend you’ve been randomly selected for audit and go through your records the way an OAE auditor would. Are all your reconciliations in order with documentation? Can you account for every dollar? This exercise can reveal weak spots before an actual auditor does. Some firms even hire an outside accountant or ethics attorney to do a “mock audit” or compliance review.

While Rule 1:21-6 doesn’t provide a formal mechanism for a voluntary audit by the OAE, the NJSBA and private consultants can offer guidance. The goal is to find and fix issues internally. If you discover a mistake (say you realize a past reconciliation never accounted for a $100 bank charge), correct it and document the correction. New Jersey regulators tend to discipline more harshly those who ignore or cover up problems versus those who proactively address them. If an audit letter arrives, you’ll feel much calmer knowing your house is already in order.

9. Communicate and educate within your firm

Ensure everyone on your team who handles client funds – partners, associates, paralegals, office managers – understands the gravity of trust accounting. Set written protocols for how trust money is received, recorded, and disbursed. For example, require that every check arriving is immediately copied and given to the bookkeeper, or that no trust check goes out without two people verifying the client balance. Regular training or reminders can enforce these habits. If you’re a solo, educate yourself: take that CLE on trust accounting, read the New Jersey OAE’s quarterly bulletins or ethics opinions. An investment in understanding the “why” behind the rules will help you implement the “how” more effectively.

By following these best practices, small and mid-sized firms can significantly reduce the risk of trust accounting missteps. Yes, it requires diligence and some investment of time (and possibly money in software or services), but the peace of mind that comes from a clean trust account is priceless. You’ll not only avoid ethical troubles, but you’ll also be able to assure clients that their funds are handled with the utmost care – which builds trust and confidence in your professionalism.

Safeguarding Your Firm Through Better Workflows

Trust accounting compliance in New Jersey might seem daunting, especially for a small firm without a full-time accounting department. But it’s entirely achievable with the right approach and tools. The key is to be proactive: implement strong procedures, leverage technology, and make trust compliance a routine part of your firm’s workflow. By doing so, you protect your clients, your law license, and your firm’s reputation. The pain points – the confusing rules, the meticulous recordkeeping, the fear of an audit – can all be addressed by putting in place a system that works with your practice instead of against it.

One effective step is to explore legal-specific accounting solutions that streamline trust management. Modern software like LeanLaw is designed with New Jersey’s trust accounting rules in mind, helping you automate three-way reconciliations, maintain immaculate client ledgers, and prevent common errors – all while integrating with your day-to-day billing and banking.

Adopting such tools can turn trust accounting from a source of anxiety into just another routine (dare we say almost easy?) part of running your firm. Imagine having your monthly reconciliation done in minutes, with confidence that every transaction is properly labeled and balanced. That frees you to focus more on your clients and less on paperwork, and it keeps you prepared if that audit notice ever comes.

In the end, compliance is not just about avoiding punishment – it’s about running a trustworthy, efficient law practice. When you have sound trust accounting practices, you give your clients peace of mind that their money is safe, and you give yourself the peace of mind that you’re meeting your ethical obligations.

So take action now: review your current trust accounting processes and identify areas to improve. Maybe it’s setting up a regular reconciliation schedule, or finally closing that old trust account with a few dollars left, or investing in software and training for your staff. Small changes can make a big difference in compliance. New Jersey’s regulators have provided plenty of guidance and clearly marked the path – it’s up to you to follow it.

By implementing better workflows and perhaps embracing tools purpose-built for law firm accounting, even the smallest firm can achieve big-firm standards in trust compliance. Don’t wait for a crisis to force your hand. Start strengthening your trust accounting today, and turn this once painful chore into a seamless part of your firm’s success story. Your future self – and your clients – will thank you.