Article Summary:

- Massachusetts lawyers face strict trust accounting rules: All client funds must be kept in special trust accounts (IOLTA or individual interest-bearing accounts) separate from firm money, per Mass. Rule 1.15. Small or short-term client funds go into a pooled IOLTA account, while substantial funds held longer must earn interest for that client in a separate account. Non-compliance can lead to ethics violations, lost client trust, and even disbarment.

- Robust recordkeeping and oversight are required: Massachusetts attorneys must maintain detailed records for each trust account (client ledgers, check registers, etc.) and reconcile balances regularly. The Board of Bar Overseers (BBO) enforces strict compliance – even unintentional mistakes like a bounced trust check can trigger an audit and disciplinary action.

- Best practices and tools simplify compliance: By segregating all client funds, doing three-way reconciliations monthly, training staff on trust accounting procedures, and using legal-specific accounting software (like LeanLaw) to automate tracking and reporting, small firms can stay compliant and avoid common pitfalls. Massachusetts offers resources like the IOLTA Committee’s guides and free BBO trust accounting trainings to help firms manage trust accounts responsibly.

Trust accounting is a critical responsibility for any Massachusetts law firm that handles client money. Mishandling client funds isn’t just a minor bookkeeping error – it’s an ethical violation that can put your license at risk. In fact, bar counsel consistently report that trust account mismanagement is one of the most frequent causes of serious disciplinary actions against lawyers. Massachusetts has its own specific rules and processes for trust accounts, including the Interest on Lawyers’ Trust Accounts (IOLTA) program and detailed requirements from the Massachusetts Board of Bar Overseers (BBO).

This guide will walk small and mid-sized firm attorneys and administrators through the essentials of IOLTA and trust accounting compliance in the Commonwealth, highlighting key rules, common challenges, and practical strategies to stay on track. We’ll also touch on how modern tools – like LeanLaw’s legal accounting software – can support your compliance efforts (without making technology the central focus).

Read on for an organized, educational overview of Massachusetts trust accounting obligations, best practices drawn from industry and ethical experts, and answers to frequently asked questions. By the end, you should have a clearer roadmap to managing client funds in compliance with Massachusetts law and avoiding the pitfalls that have tripped up many well-intentioned lawyers.

What Is IOLTA and Why Does It Matter in Massachusetts?

“IOLTA” stands for Interest on Lawyers’ Trust Accounts – a program mandated in Massachusetts (and all U.S. jurisdictions) to ensure that client funds which are nominal in amount or held short-term don’t sit idle. Massachusetts Rule of Professional Conduct 1.15 requires attorneys to deposit client money in interest-bearing accounts. If a client’s funds are too small or will be held too briefly to generate net interest for that client, they must go into a pooled trust account where the interest is donated to the public good.

In Massachusetts, that pooled account is an IOLTA account, and the interest earned is remitted to the Massachusetts IOLTA Committee, which distributes the funds to legal aid organizations and justice programs across the state. Essentially, IOLTA turns pennies of interest into funding for access to justice – a win-win that allows lawyers to hold client funds without unjust enrichment, while benefiting society.

Every lawyer in Massachusetts who holds client funds in trust needs an IOLTA account, unless those funds are significant enough to warrant a separate account for the individual client. The Massachusetts IOLTA Committee’s guidelines make this clear: it’s the attorney’s good-faith judgment that determines whether funds are “nominal or short-term” (go into IOLTA) or large/long-term (go into a separate interest-bearing trust account for the client).

For example, typical IOLTA-appropriate funds include small retainers or advance fee deposits, settlement proceeds awaiting disbursement, and similar client monies you might hold only briefly. By contrast, if you’re holding a six-figure sum for a year-long escrow, that should probably be in a segregated account where the client (not IOLTA program) gets the interest.

Why does IOLTA matter? Beyond its charitable mission, using an IOLTA or proper trust account is legally required and is fundamental to your fiduciary duty. It ensures client funds are segregated from the firm’s money at all times, preventing even the appearance of impropriety. Remember, client money is not your money – you hold it only in trust, and misusing it (even inadvertently) is a grave offense.

Massachusetts ethics rules make it clear that failing to safeguard client funds – whether by commingling them with operating funds or not accounting for them properly – can lead to severe penalties. In short, an IOLTA account isn’t just a bureaucratic requirement; it’s a critical tool to protect clients’ property and maintain the integrity of your law practice.

(Fun fact: Massachusetts has over 14,000 IOLTA accounts across more than 200 banking institutions statewide. If you handle client funds, you’ll be joining just about every law firm in the state in participating in the IOLTA program.)

Massachusetts Trust Accounting Rules and Requirements

Massachusetts has strict trust accounting rules that govern how you must handle client funds. These rules are primarily found in Mass. R. Prof. C. 1.15 (Safekeeping Property) and are enforced by the Board of Bar Overseers. They cover everything from where you can bank your trust funds to exactly how to record and reconcile every transaction. Below, we break down the key Massachusetts-specific requirements you need to know:

Setting Up the Proper Trust Account (IOLTA or Separate Trust)

When you receive client funds, the first step is making sure they’re deposited into the correct type of account:

IOLTA Accounts for Nominal/Short-Term Funds

As noted, if the funds are small in amount or will be held only briefly, they go into your pooled IOLTA account. Massachusetts attorneys in private practice must open an IOLTA account at an approved bank as soon as they first receive such client funds. The account should be clearly titled as a trust account (e.g., “XYZ Law Firm IOLTA Trust Account”) – in fact, by rule the account name must include words like “Trust Account,” “Client Funds Account,” or “IOLTA” to signal its purpose.

You’ll need to use a bank that’s been certified by the Massachusetts IOLTA Committee (see the Committee’s list of eligible banks) and is FDIC-insured. When opening the account, file a Notice of Enrollment (NOE) with the IOLTA Committee – this registration notifies them of your new IOLTA account so the bank can begin remitting interest to the program. (Fortunately, the NOE can be submitted online, and you no longer have to mail a form.) Massachusetts requires that all IOLTA accounts be held in-state, so your IOLTA must be with a Massachusetts bank unless you get specific client consent to use an out-of-state institution.

Individual Trust Accounts for Significant/Long-Term Funds

If a client entrusts you with a large sum or funds to hold for a long duration, Massachusetts expects you to open a separate interest-bearing account for that client (with the interest payable to the client) rather than putting it in IOLTA. This typically comes up with hefty settlement escrows, real estate transaction funds, or long-term escrow arrangements. Opening a separate trust account will require the client’s tax ID info (so the bank can assign interest income to them) and, under Mass. rules, you must notify the BBO when you open such an account (the BBO provides forms for this).

All the same trust accounting rules apply to these individual accounts (recordkeeping, no commingling, etc.), except that the interest goes to the client. Tip: Clearly document your decision process for choosing an IOLTA vs. individual account. Rule 1.15(e) gives lawyers discretion, but you should be able to show you exercised good faith judgment about what’s “nominal or short-term.” The 2009 Massachusetts IOLTA Guidelines offer factors to consider (e.g., the amount of interest that could be earned versus the cost of setting up a separate account).

Importantly, all trust accounts – whether IOLTA or individual – must be maintained at a financial institution that has agreed to comply with Massachusetts’ trust account regulations. Banks on the IOLTA Committee’s approved list have done so. Among other things, these banks agree to notify bar counsel if a trust check is dishonored (Massachusetts, like many states, has a “dishonored check rule” requiring overdraft/bounce notifications to the BBO). In practical terms, this means if you accidentally bounce a check or dip below zero in your trust account, bar counsel will find out about it – a strong incentive to stay vigilant with your trust bookkeeping! (More on reconciliations and avoiding overdrafts below.)

No Commingling of Funds – Ever

Commingling is the cardinal sin of trust accounting. It means mixing client funds with your own funds or law firm funds in the same account. Massachusetts flatly prohibits this. All client money must be kept separate from the lawyer’s money. The only wiggle room is that you’re allowed to keep a small amount of your own money in the trust account solely to cover bank service charges – typically a few hundred dollars at most. Beyond that, none of your operating funds should be in the trust account, and vice versa.

What about money that is partly yours and partly the client’s? For instance, a client pays a $10,000 advance, and you will earn portions of it over time. Massachusetts handles this by requiring it all to go into trust, and then you withdraw your earned fees promptly when they are earned. You cannot leave earned fees sitting in trust indefinitely (that would be commingling once they’re yours), but you also cannot take them out before they are earned (that would be converting client property).

In practical terms, if you bill $2,000 of work against that $10,000 retainer, you would invoice the client and then transfer $2,000 from trust to your operating account – at that point, that $2,000 is no longer client property. The remaining $8,000 stays in trust until more fees are earned or a refund is due.

Massachusetts’ rules also address scenarios of disputed funds: if there’s a dispute over fees or who owns funds, the disputed amount must remain in the trust account until the dispute is resolved. For example, if a client contests a bill and refuses to consent to your withdrawal of fees, you cannot unilaterally take the contested portion – that money stays in trust (and you might seek resolution through fee arbitration or other means). By contrast, any undisputed portion can be withdrawn and paid out.

Finally, never “borrow” from one client’s money to pay another, even briefly. In a pooled IOLTA account, this translates to: you must never let any individual client’s sub-account go negative, even if the overall account balance is positive. If client A’s funds are used (even momentarily) for client B’s bills, you’ve effectively commingled clients’ funds and engaged in an unauthorized loan – a serious breach. Each client’s funds are sacrosanct for that client’s matters only.

Timely Deposits and Disbursements Only for Proper Purposes

All client funds qualifying as trust funds should be deposited promptly. Massachusetts expects that any client or third-party funds you receive in connection with legal services will be deposited without delay into a trust account. For instance, if you receive a settlement check on a client’s behalf or an advance fee payment, get it into the trust account as soon as reasonably possible (the Massachusetts IOLTA Committee suggests that deposits should ideally be made daily). This protects the funds and ensures they are covered by FDIC insurance, etc.

Conversely, you should only disburse (pay out) money from a trust account for a proper purpose – i.e., to pay the client or on the client’s behalf, or to pay yourself fees that you’ve earned pursuant to your fee agreement. Every withdrawal of fees by the lawyer must be properly documented. Massachusetts explicitly requires that on or before the date you withdraw fees from trust, you must give the client an invoice or an accounting showing what fees have been earned and the balance remaining in trust after the withdrawal.

In other words, you can’t quietly dip into the trust account; you need to bill the client (or otherwise notify them) and make a record. Additionally, you cannot use the trust account to pay personal or firm expenses – e.g., you wouldn’t pay your office rent directly from an IOLTA account. Only client-related disbursements (settlement payouts, filing fees, client refunds, etc.) or transfers to your operating account for earned fees are appropriate.

Prohibited transactions

Massachusetts’ rule 1.15 has a few bright-line prohibitions to prevent stealth or sloppy withdrawals. You cannot withdraw trust funds using any method that hides the recipient. For example, writing a trust account check made out to “Cash” or “Bearer” is forbidden. Likewise, you can’t withdraw cash from a trust ATM or make electronic transfers out that don’t document a recipient. Every disbursement should be by a check or electronic transfer payable to a specific payee so there’s a clear paper trail.

All checks must be pre-numbered (no unnumbered counter checks that are hard to track). These measures are there to ensure accountability: if every check is numbered and made out to a named party, it’s much harder for funds to go missing or for someone to siphon off money undetected.

One more Massachusetts-specific point: Advances for expenses (like a client gives you money to cover filing fees or investigator bills) should also be handled through trust. In some states, lawyers can put advances for costs in the operating account since those are not fees for the lawyer. But Massachusetts’ rules, updated in 2015, clarified that advances for costs must also be treated as client funds and kept in trust. So don’t deposit a client’s $500 advance for court fees into your business account – it belongs in IOLTA until you pay the court, at which point you’d disburse that amount to the court or reimburse yourself if you fronted the payment.

Detailed Recordkeeping (and 6-Year Record Retention)

Perhaps the most labor-intensive (but crucial) aspect of trust compliance is recordkeeping. Massachusetts requires contemporaneous, complete records of all receipts, disbursements, and balances for client trust funds. In practice, this means you need to maintain at least:

- A Master Trust Account Check Register: This is the running checkbook for the trust account, showing every deposit and withdrawal in chronological order, with dates, amounts, check numbers, payees, etc., and the current balance after each transaction. Think of it as the checkbook ledger for the account as a whole.

- Individual Client Ledgers: A separate record for each client (or client matter) that shows all the transactions for that client’s funds and the current balance held for them. Every time you deposit money for Client X or pay something out for Client X, it should reflect on Client X’s ledger. The ledger should never go negative (that would indicate you paid out more for that client than you had for them). If you have a pooled IOLTA, these individual ledgers are critical to keep track of each client’s share of the account.

- Account Documentation: Basic account identifying info (bank name, account number, account title) and account statements from the bank. You should have monthly bank statements for the account and any related documents like canceled check images or deposit slips. Massachusetts also specifically wants you to note whether an account is IOLTA or individual and the opening/closing dates.

- Duplicates of Deposits and Checks: It’s good practice (and implicitly required by the “records of receipts and disbursements” language) to keep copies of all deposit receipts, checks you issued, wire transfer confirmations, etc. For every transaction, there should be some supporting document. Many attorneys use duplicate checks or check scanners to retain images.

- Records of Attorney Funds for Bank Fees: If you do keep a small $100-$200 of your own funds in the account for bank fees, Massachusetts expects a ledger for that as well, to track that “cushion” amount. This helps prove you’re only using it for bank charges and not mixing in more of your money.

All these records must be kept for at least six years after the representation ends or the trust account closes (whichever is later). Practically, many firms keep trust records much longer (scanning them for permanent storage) because questions can arise years down the line. The rule is six years minimum, so be sure not to toss old trust ledgers or bank statements too soon.

Massachusetts has embraced electronic recordkeeping – you can keep these records in digital form as long as they can be printed on demand and you have a reliable backup system. For example, maintaining your client ledgers in a practice management software or spreadsheet is fine, but you should regularly back up the data (and likely keep a PDF or hard copy of periodic reports). The key is that if the BBO audits you, you can produce a complete record of all trust transactions and balances.

One more requirement: regular client notifications and accountings. Massachusetts Rule 1.15 also requires that you notify clients or third-party beneficiaries when you receive funds or property on their behalf, and upon request, provide a full accounting. In everyday terms, if you receive a settlement check, let the client know it arrived. If you’re holding money and the client asks for a breakdown of what’s there, you must promptly give them an up-to-date ledger or accounting.

And certainly, when you finalize a matter, provide the client with a trust balance reconciliation and return any remaining funds with a closing statement. Good communication here not only keeps you compliant but also helps avoid misunderstandings. Clients should never be in the dark about money you’re holding for them.

Regular Reconciliation of the Trust Account

Maintaining the ledgers and registers is only half the battle – you also need to reconcile the trust account regularly. Reconciliation means making sure that your internal records match the bank’s records, and that the funds you’re holding for clients align perfectly with the total in the account. Massachusetts requires that trust accounts be reconciled no less frequently than every 60 days. Best practice (and the expectation of bar counsel) is to do it monthly, which makes it easier to catch and correct errors.

What does a reconciliation entail? In Massachusetts, if you have a pooled trust account holding funds for multiple clients, you need to do a three-way reconciliation. This means you prepare a report showing three things side-by-side:

- The balance according to the bank statement (adjusted for any outstanding checks or deposits not yet reflected by the bank).

- The balance according to your checkbook register (your running trust account balance in your records).

- The total of all individual client ledger balances (adding up the balances of every client’s sub-account).

All three of those numbers must be identical. If they aren’t, something is off – maybe a transaction was recorded in one place and not another, or the bank charged a fee you didn’t log, etc. You must investigate and resolve any discrepancies. Massachusetts specifically mandates this type of reconciliation for any account with more than one client’s funds. (If an account is truly dedicated to a single client matter, you can reconcile just bank vs. register, but in practice it’s wise to still document that.)

Performing these reconciliations regularly is your best protection against trust accounting errors. It can catch, for example, a check printing error, a bank service charge that accidentally hit your account, a math mistake in your ledger, or even someone tampering with funds. Many disciplinary cases have started because an attorney failed to reconcile and didn’t notice a problem until it snowballed – by reconciling monthly, you’ll spot issues early when they’re easier to fix.

Tip: Document each reconciliation with a dated report or worksheet and keep those reports for 6 years as part of your records. The rule actually requires you to retain reconciliation reports. If you use software like QuickBooks or LeanLaw, you can generate a trust reconciliation report each month and save it. The BBO’s trust inspection team will want to see those if you’re ever audited.

Oversight by the BBO and Consequences of Non-Compliance

The Massachusetts Board of Bar Overseers (BBO), through the Office of Bar Counsel, monitors and enforces trust accounting compliance. Attorneys are subject to discipline if they violate Rule 1.15 – and the consequences can be severe. Sanctions range from informal admonitions (for minor, isolated recordkeeping lapses) to public reprimands, suspensions, or disbarment for serious misuse of client funds. Massachusetts courts have repeatedly stated that the misuse or neglect of client funds jeopardizes the public’s trust in the profession and thus is treated very seriously.

A few sobering points and trends:

- The BBO runs a Trust Account Overdraft Notification Program in conjunction with banks. If any trust account check bounces or if your account goes into the red (beyond any tiny bank buffer), the bank will send a notice to bar counsel. Many attorneys have received that dreaded letter from bar counsel asking for an explanation – or even opening an investigation – all because of an overdraft. Often, even “innocent” mistakes (math errors, bank errors, forgetting to record an ACH fee) that cause an overdraft will lead to scrutiny. It’s far better to prevent these issues than to have to explain them after the fact.

- Misappropriation (intentionally taking client money) almost always results in disbarment. But even unintentional mismanagement can lead to discipline. For example, repeated failure to reconcile or consistently using one client’s funds to cover shortfalls for another (even without personal gain) can result in multi-month suspensions. The statistics bear out that trust accounting violations are disproportionately represented in disciplinary cases – many ethics complaints involve some element of poor trust management.

- Massachusetts bar counsel also spot-checks compliance in other ways. If a client complains about something unrelated but it comes out that your trust records are a mess, bar counsel may expand an investigation. In some instances, random audits have been known to occur, especially for new solo practitioners, to ensure understanding of trust rules. The BBO also offers a free Trust Account Training program (monthly via Zoom) – in fact, attendance is sometimes required as part of a disciplinary resolution for those who’ve had issues. Proactively attending this training is a great idea for any lawyer new to trust accounting (and for staff!), as it covers recordkeeping “traps for the unwary” and best practices.

In short, not paying attention to trust compliance is simply not an option if you want a healthy law practice. The good news is that by following the rules outlined above and implementing prudent systems and habits, you can stay well within the bounds and greatly reduce any risk of disciplinary trouble.

Best Practices for Trust Account Compliance in Your Firm

Staying compliant with Massachusetts trust accounting rules might sound daunting, but it boils down to consistent good practices and internal controls. Here are some industry-recommended best practices (drawn from legal ethics opinions, bar resources, and practice management experts) to help your firm avoid common trust accounting pitfalls:

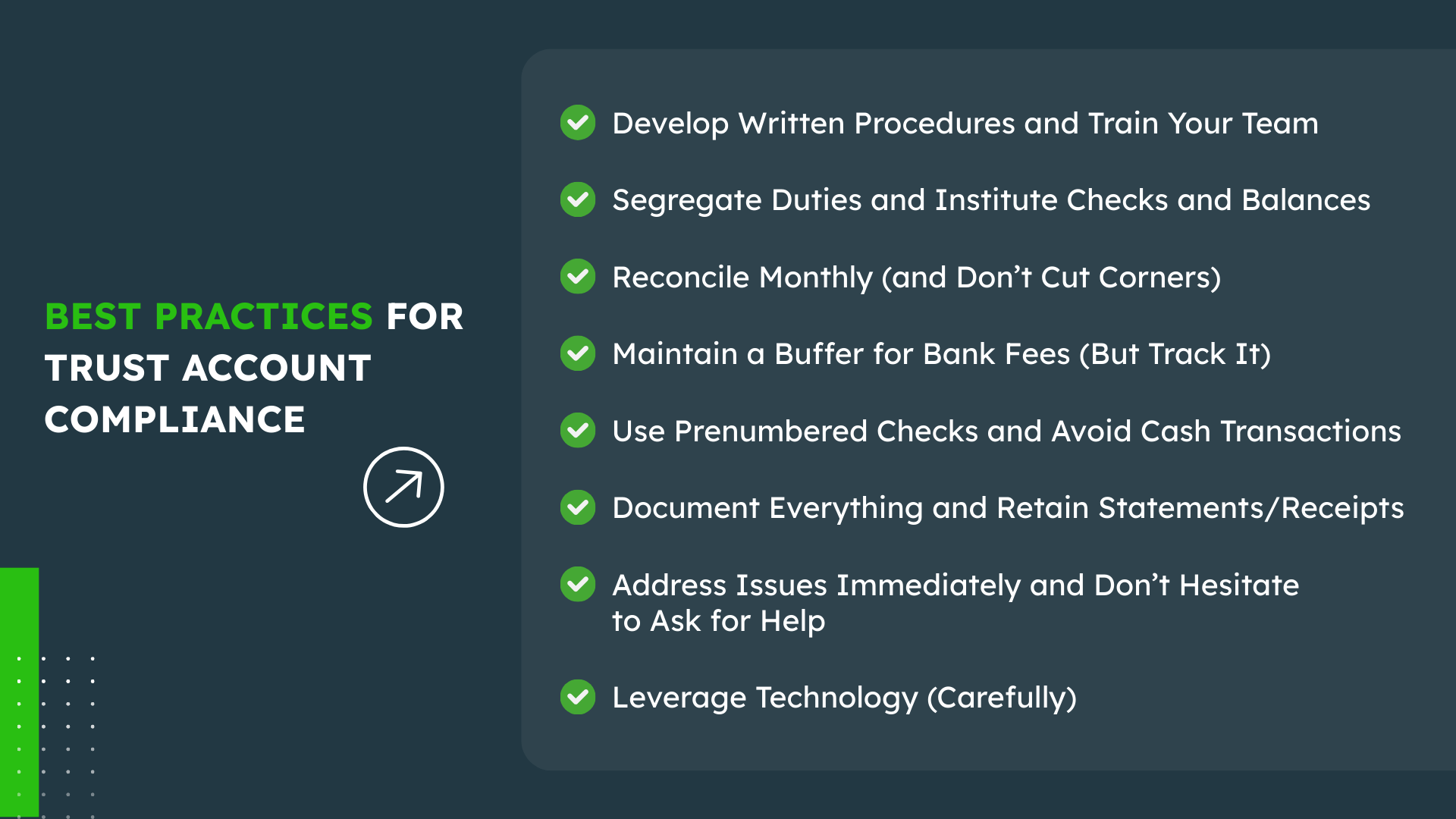

- Develop Written Procedures and Train Your Team: Don’t assume everyone intuitively knows how to handle trust funds. Create a simple internal handbook or checklist for trust account operations – covering how to receive funds, deposit them, record transactions, make withdrawals, etc. – and train every lawyer and staff member who might touch the trust account on these procedures. Emphasize the do’s and don’ts (for example, no commingling, no checks to cash, always get a supervisor’s approval before withdrawing client funds). Given staff turnover and the involvement of non-lawyer bookkeepers or assistants, continuous training is key. The goal is to build a culture where everyone understands that proper trust accounting is non-negotiable. Massachusetts bar counsel Constance Vecchione once noted that inadequate training and oversight is a major factor in many trust account violations – so get ahead of that by educating your team.

- Segregate Duties and Institute Checks and Balances: In a small firm it may be hard to have full separation of roles, but aim for some level of internal oversight. For example, if one person (say a bookkeeper) prepares the trust reconciliation, have another person (the managing partner or a second attorney) review and sign off on it monthly. Two pairs of eyes on the trust records can catch mistakes or irregularities. You might also require that any check above a certain amount needs two signatures, or at least notice to a second person. The idea is to create accountability so that no single individual has unchecked control over client funds. This protects against both errors and intentional misdeeds, and it also helps instill firm-wide responsibility for compliance.

- Reconcile Monthly (and Don’t Cut Corners): Treat the monthly three-way reconciliation as sacrosanct. Set a recurring calendar reminder for a few days after each bank statement is available. When reconciling, actually produce the report showing the bank, check register, and client ledger balances side by side. If any differences arise, investigate immediately – it could be something like a $20 bank fee or a recording delay, which you can then fix and document. By reconciling every month, you also make the eventual year-end accounting or any audit much less painful. Remember, Massachusetts requires at least every 60 days; make it easier by doing it every 30 days. Pro tip: Many lawyers find it helpful to have a second person review the reconciliation (or at least review the client ledger balances) to ensure nothing looks off. And if you find the reconciliation process cumbersome, that’s a sign you might benefit from software tools (see below) to streamline it.

- Maintain a Buffer for Bank Fees (But Track It): It’s acceptable (indeed advisable) to keep a small amount of firm money in the trust account to cover unforeseen bank charges – e.g., a monthly maintenance fee or wire transfer fee – so that such charges don’t accidentally dip into client funds. Massachusetts permits this as an exception to commingling. However, treat that buffer as a buffer only. Keep a ledger for those firm funds and review it periodically. If the bank fees have eaten it up, replenish it from the operating account. Never use client money to pay bank charges. And the amount should be modest; if you have thousands of your own dollars sitting in IOLTA “just in case,” bar counsel might view that with suspicion.

- Use Prenumbered Checks and Avoid Cash Transactions: This is already a rule, but it’s worth restating as a best practice. Ensure your trust account checkbook uses prenumbered checks (most business checkbooks do by default) and never use starter checks or counter temporary checks that aren’t traceable. Also, do not use the ATM card for the trust account (better yet, don’t even request one). All movements of money should go through properly documented checks or electronic transfers that leave a paper trail with recipient details. These habits prevent a lot of trouble – you’ll always know what a withdrawal was for, and you minimize the risk of theft or loss of funds.

- Document Everything and Retain Statements/Receipts: Make it a habit that every trust deposit or withdrawal has backup documentation. For deposits, this could be a copy of the check and a receipt from the bank or a screenshot of the electronic deposit confirmation. For disbursements, keep a copy of the issued check (your accounting software or bank can provide images) or wire confirmation, plus the client invoice or instruction authorizing the disbursement. For any online transfers, print the confirmation screen or email. Store these digitally in a “Trust Receipts and Disbursements” folder organized by month or client. Having complete documentation not only keeps you compliant with Rule 1.15’s record requirements, but also makes it vastly easier to answer any client or auditor questions. The LeanLaw blog’s Legal Trust Accounting Compliance Checklist provides a helpful summary of records to keep and points to verify (like always recording the source, amount, purpose, and client for each transaction). It’s wise to review such a checklist periodically against your own practices.

- Address Issues Immediately and Don’t Hesitate to Ask for Help: If you do spot something wrong – say you discover a client ledger went negative due to a mis-applied deposit, or you realize a bank error – address it immediately. Don’t let unknown discrepancies linger. It may be as simple as transferring firm funds in to correct a shortfall (if, for example, a bank charge accidentally hit the account and you need to reimburse it) or reaching out to the bank to fix an error. Massachusetts has mechanisms for dealing with certain problems (e.g., if you genuinely cannot find the owner of some unclaimed funds despite diligent search, the rules now allow transferring such funds to the IOLTA Committee after a period of time ([PDF] The Supreme Judicial Court’s Standing Advisory Committee on the …)). If you’re unsure how to handle a trust accounting issue, seek guidance – the Massachusetts IOLTA Committee and the Office of Bar Counsel are resources, and there are ethics hotlines and consultants who specialize in trust accounting. It’s far better to show that you proactively sought to fix a problem than to ignore it and hope no one notices.

- Leverage Technology (Carefully): In 2025, you don’t have to manage trust accounts with just a manual ledger and abacus. There are excellent software tools designed to make trust accounting easier and less error-prone. For instance, legal-specific accounting software like LeanLaw (which integrates with QuickBooks Online) can automate many compliance safeguards – it will keep client ledger balances for you, prevent common mistakes like ledger overdrafts, and even produce three-way reconciliation reports on demand. Using software doesn’t relieve you of responsibility, but it can significantly reduce the tedious work and the risk of human error. That said, any technology is only as good as the user: be sure to properly set up your accounts in the software and still review the output. Many Massachusetts firms have found that by adopting a modern practice management system that includes trust accounting features, they save time and gain peace of mind. You can read more about implementing IOLTA accounting in QuickBooks in LeanLaw’s blog post on Managing IOLTA in QuickBooks Online, which offers step-by-step best practices. In short, don’t shy away from tech – the right tools can enforce separation of funds, automate your tracking, and remind you of tasks like reconciliations.

By following these best practices, you’ll not only adhere to the letter of Massachusetts law but also create an internal system where compliance is almost second-nature. The goal is to make it hard to do it wrong and easy to do it right – through training, systems, and a little help from technology. As a bonus, good trust accounting practices often correlate with better overall financial management in your firm (e.g., you’ll bill timely to withdraw your fees, you’ll know exactly what retainers you have on hand, etc.). It’s truly a foundation for both ethical and fiscal health in a law practice.

How Legal Software Like LeanLaw Supports Trust Compliance

Managing all these trust accounting duties can be time-consuming, but legal software can lighten the load. Modern practice management and accounting tools are built with compliance in mind. For example, LeanLaw’s trust accounting software is designed to help law firms meet state bar requirements with less effort. It works as an overlay to QuickBooks Online, creating a seamless legal-specific accounting system. Here are a few ways technology like LeanLaw can support your Massachusetts trust compliance:

- Dedicated Trust Accounting Features: Unlike generic accounting software, legal-specific tools understand concepts like client ledgers and trust balances. In LeanLaw, you set up a designated trust bank account (or multiple) and record client deposits into it. The software automatically maintains a subledger for each client – so at any time you can see how much money you hold for Client A, Client B, etc. This prevents the common error of commingling client funds or losing track of who has what. Every invoice payment or retainer is tied to a client matter, ensuring that you always know exactly which client’s funds are in trust and in what amount.

- Automated Three-Way Reconciliation: One of the standout features of tools like LeanLaw (integrated with QuickBooks) is the ability to do rapid reconciliations. The software can generate a reconciliation report that compares your bank balance, your trust ledger in QuickBooks, and the sum of all client balances – the required three-way reconciliation. It flags any discrepancies so you can fix them. Instead of manually cross-checking spreadsheets and bank statements, you can reconcile with just a few clicks each month. This not only saves time but also serves as a built-in reminder to actually perform the reconciliation. LeanLaw, for instance, bakes reconciliation into its workflow, nudging you to do it and producing the needed reports.

- Comprehensive Reporting and Audit Trails: Good software will let you easily pull all the reports that a regulator or client might ask for. With a tool like LeanLaw, you can at any moment generate a client trust ledger report (showing every transaction for that client’s funds), a list of all client trust balances, or a transaction history for the trust account. If a client needs an update or if you were audited, you could produce the required information in minutes, without digging through paper files. Some software even allows you to attach documents (like scanned checks or deposit slips) to each transaction, so you have one-click access to the proof behind each entry. This creates a strong audit trail.

- Controls and Permissions: In a multi-user environment, software can enforce user permissions to add internal controls. For example, LeanLaw lets firms set up approval workflows – a paralegal could enter a disbursement, but it won’t actually sync to QuickBooks until a partner approves it. You can restrict who can actually move money versus who can view reports. These settings act as a safeguard against unauthorized transactions, complementing your internal policies.

In summary, while you as the attorney are ultimately responsible for trust compliance, using purpose-built software is like having an extra layer of security and efficiency. It handles the heavy lifting of calculations, prevents many mistakes before they happen (e.g., warning you if a ledger would go negative), and keeps your records organized. Many small and mid-sized firms in Massachusetts are now leveraging such tools to simplify IOLTA accounting – freeing up time to focus on clients while staying confident that their trust account is accurate to the penny. (For a deeper dive into trust accounting software benefits, check out our overview in the LeanLaw blog’s Trust Accounting Guide or schedule a demo to see these features in action.)

Massachusetts IOLTA & Trust Accounting FAQ

Below we answer some frequently asked questions about trust accounting in Massachusetts, to reinforce key points and clear up common areas of confusion:

Q: What is an IOLTA account, and who needs to have one in Massachusetts?

A: An IOLTA account is a special, pooled interest-bearing trust account for client funds. In Massachusetts, any attorney who holds client funds that are “nominal in amount” or to be held short-term is required to have an IOLTA account. Essentially, if you ever handle retainers, settlement proceeds, escrow deposits, or any client money that won’t immediately be distributed, you must deposit it into an IOLTA (unless it’s a large sum expected to earn significant interest for the client, in which case you’d set up a separate account for that client).

The IOLTA account must be at an approved Massachusetts bank, and you must register it with the Massachusetts IOLTA Committee. The bank will send any interest earned to the IOLTA Committee (you or the client do not get the interest). If you’re a Massachusetts-licensed lawyer practicing in-state, not having an IOLTA when you hold client funds would violate the rules. (Exceptions are very limited – e.g., if you never deal with client money, or you practice out of state with no Massachusetts office.) For most small firms, assume you need an IOLTA. It’s both a compliance requirement and an ethical safeguard for handling client property.

Q: What types of funds go into a trust account versus the law firm’s operating account?

A: The guiding principle is: client or third-party funds in your possession go into a trust account, unless they are fully earned fees or reimbursement. If the money is in advance of work (unearned) or is for a client expense or belongs to someone else, it belongs in trust. Common examples that must be deposited into trust include: advance fee retainers, flat fees paid upfront (until you perform the services over time), settlement funds you’re holding before disbursement, escrow funds for a transaction, or money a client gives you to pay filing fees or other costs.

These are all client funds. None of that should go into your firm’s operating account until it’s earned or expended for the client. By contrast, funds that are your earned fees or reimbursements can go into your operating account – but only after they are earned. For example, once you’ve completed work billed against a retainer and the client approves an invoice, you would transfer that amount from trust to operating. Similarly, if you incur costs and bill the client for reimbursement from their trust deposit, you can move that amount to operating when billing.

But you should never deposit a check that includes any unearned portion directly into operating. A helpful way to think of it: if you might have to give the money back or spend it on the client’s behalf, it should be in the trust account, not commingled with the firm’s funds. Massachusetts rules explicitly state that legal fees paid in advance must be held in a trust account and withdrawn only as earned. The only funds of yours allowed in trust are a minimal amount for bank charges or any portion of a fee that’s earned and not disputed (and even then, you should remove earned fees reasonably promptly).

Q: How often do I need to reconcile my trust account, and what does that involve?

A: Under Massachusetts Rule 1.15, you must prepare a reconciliation of each trust account at least every 60 days. In practice, the BBO expects monthly reconciliation as the standard (and it’s considered a best practice to reconcile monthly). Reconciling means making sure your three balances match: (1) the bank statement balance (adjusted for any outstanding checks/deposits), (2) your internal check register balance, and (3) the total of all client ledger balances.

A “three-way” reconciliation ensures you haven’t missed recording any transactions and that no client’s funds are unaccounted for. Each time you reconcile, you should generate a report or document showing these three balances are identical. If you find a discrepancy – say your register is off by $100 compared to the bank – you need to find and fix the error (common issues are a transaction recorded in one place and not the other, math mistakes, or bank fees not recorded).

Also, if you have multiple trust accounts (for different purposes or separate client accounts), reconcile each one separately. Be sure to keep copies of each reconciliation report as part of your six-year records archive. Many firms use software (like QuickBooks or LeanLaw) to make reconciliations easier, but even if done by hand, it’s critical to do it regularly. Not reconciling is a recipe for eventually losing track of funds – and it’s one of the first things bar auditors will ask for if you ever get a compliance audit.

Q: What specific records am I required to keep for my trust accounts, and for how long?

A: Massachusetts requires lawyers to maintain complete records of all trust account activity for each client matter and each account, for a minimum of six years after the representation ends. Key records include:

- A check register for each trust account (showing every deposit and withdrawal, with dates, amounts, payees, and running balance).

- Individual client ledgers for each client or matter with trust funds (showing all transactions for that client and the balance after each).

- Bank statements for each month, plus canceled checks (or images) and deposit slips.

- Copies of all deposit receipts and withdrawal instruments (e.g. wire confirmations, instructions authorizing disbursements, etc.). Essentially, any document related to a trust transaction should be retained.

- Any reconciliation reports you generate (the three-way reconciliation reports discussed above).

- If you keep a small amount of personal funds in the account for bank fees, a ledger for those funds.

These records can be maintained digitally, but make sure they are backed-up and can be printed on paper if needed. The six-year clock runs from the termination of the representation and the full disbursement of funds – so if you close a client matter in 2025 but still hold some of their funds until 2026, the six years would start after 2026 when the funds are fully distributed. In practice, it’s wise to just keep these records indefinitely if you can (storage is cheap).

Importantly, Massachusetts also requires that you promptly produce these records to the BBO if requested in a compliance inquiry. So having them well-organized is in your interest. Many law firms use the annual client trust account certification (if applicable) as an opportunity to audit their records. For a handy overview, see the LeanLaw Trust Accounting Compliance Checklist, which outlines the key pieces of information you need to track for every deposit and disbursement (date, amount, source, purpose, client, etc.).

Q: Can I pay bank fees or credit card processing fees out of a client’s trust funds?

A: No. Bank service charges or payment processing fees should never be deducted from client funds. Massachusetts allows lawyers to deposit a small amount of their own money into the trust account specifically to cover bank fees like monthly maintenance charges, wire fees, check orders, etc..

That way, if the bank imposes a fee, it draws from your funds, not the client’s. You should periodically replenish this if needed, and keep a record of those funds. As for credit card processing fees: If a client pays a retainer by credit card, the processing fee taken by the vendor cannot come out of the client’s money in trust. There are two ways firms handle this: either (1) use a credit card processor that allows the fee to be charged to your operating account while the full gross amount goes into trust, or (2) promptly replace the fee amount with firm funds.

For example, if a client pays $1,000 and the processor takes a $30 fee, you should deposit the full $1,000 to trust (some processors will advance the fee from your operating by default), or if only $970 hits the trust account, immediately transfer $30 from your operating account to trust to cover the shortfall. The bottom line is the client’s trust ledger should be credited with the full $1,000 they paid, and the firm should absorb the $30 cost of getting paid.

Ethically, you can charge the client for credit card fees (if disclosed), but even then, you’d charge it as an additional fee and not simply skim it from the trust deposit. It’s critical to ensure that processing fees or any similar charges do not deplete client funds – otherwise you’re effectively using client money to pay your business expense, which is improper. Using payment solutions designed for law firms (LawPay, LexCharge, etc.) can help with this, as they know how to route fees appropriately to avoid trust account impact.

Q: What happens if I make a mistake on the trust account? Will I automatically be in trouble?

A: Honest mistakes can happen, and the BBO does recognize the difference between technical errors and intentional misuse – but it’s vital to catch and correct any mistakes quickly. If, for example, you realize you wrote a trust check from the wrong client ledger or forgot to record a transaction, fix it as soon as you discover it and document what you did to remedy it. Small accounting errors that are promptly remedied (with no client harm) often result in no discipline or just an informal warning, especially if you self-report them or address them before any harm.

However, if a mistake leads to an overdraft or comes to light through a client complaint or audit, bar counsel will expect an explanation of how it happened and what you’ve done to prevent a recurrence. Patterns of neglect (like repeatedly failing to reconcile or multiple bounced checks) will be viewed much more harshly than a one-time slip that you handled responsibly. The key is not to hide problems.

If you uncover a significant issue – say a trust shortage – you may want to consult ethics counsel on whether self-reporting to bar counsel is advisable. Massachusetts has an ethic of self-reporting serious issues (for example, if you find out a employee misused funds, it’s often best to notify bar counsel and make the client whole immediately, which can mitigate discipline). In summary, a mistake is not automatically career-ending, but ignoring a mistake or not having proper systems (so that mistakes happen often) can certainly lead to disciplinary trouble. This is why those best practices of reconciliation and oversight matter – they help you catch mistakes when they are still molehills, not mountains.

Q: How can a small firm without a dedicated accountant effectively manage trust compliance?

A: Small firms often don’t have the luxury of a full-time accountant or administrator focusing on trust accounting, but they can still achieve compliance by leveraging planning and technology. First, assign one attorney as the primary person responsible for the trust account – often the managing partner or a conscientious lawyer in the firm. Make it part of their duties to oversee trust reconciliations and educate others. Next, consider using software tools (like LeanLaw with QuickBooks Online, or other legal accounting software) which are essentially your “extra staff member” for bookkeeping.

These tools can automate many tasks: tracking each client’s balance, alerting you to errors, and preparing reports. For example, LeanLaw’s integration can automatically separate client payments into operating vs trust accounts as needed and keep a running ledger, saving you manual math. Even with software, you should regularly review what it’s doing – but it dramatically cuts down on tedious work and the chance of human error. Additionally, take advantage of resources like the Massachusetts BBO’s free trust accounting training seminars – they are often just an hour long and packed with practical tips.

You can also find checklists and guides (the IOLTA Committee’s Client Funds Manual and various Massachusetts Bar Association articles) that break down the tasks. In a nutshell, even without dedicated staff, a combination of (1) clear monthly routines (deposits, updates, reconciliation), (2) good software, and (3) willingness to learn the basics will go a long way. Many small firm lawyers successfully manage their trust accounts solo – it’s doable if you stay organized. And if you ever feel overwhelmed, you can hire a part-time bookkeeper with law firm experience to review your trust records quarterly, just to double-check you’re on target. Think of it as a modest investment to avoid a very costly problem.

Trust accounting may not be the most glamorous part of practicing law, but in Massachusetts it is absolutely integral to running a compliant and successful firm. By understanding the specific requirements – from IOLTA setup and recordkeeping to reconciliation and client communication – and by implementing strong habits and tools, you can keep your client’s funds safe and your firm out of hot water.

The Massachusetts bar authorities want you to succeed at this: plenty of guidance is available, and modern software like LeanLaw exists to assist you in getting it right. Small and mid-sized firms can especially benefit from these efficiencies, ensuring that even without large administrative teams, they can meet or exceed the standards set by Rule 1.15. By treating every client dollar as a sacred trust, and by building compliance checks into your workflow, you’ll protect your clients, your reputation, and your license – and that’s worth every bit of effort.

For more insights on legal accounting and practice management, explore the LeanLaw Blog which offers articles on trust accounting best practices, technology tips, and more. And whenever in doubt, remember the golden rule of trust funds: it’s not your money, and you can’t go wrong by taking meticulous care of it.